In 2026, the landscape of personal finance and healthcare continues to evolve rapidly. For many Americans, securing financial stability against life’s unpredictable challenges remains a top priority. While traditional life insurance provides a crucial safety net for loved ones after you’re gone, a growing number of policies now offer an equally vital component: living benefits. This innovative feature transforms a conventional death benefit into a versatile financial tool you can access during your lifetime, particularly when facing significant health crises. Understanding how life insurance with living benefits works can fundamentally change how you plan for your financial future, providing peace of mind not just for your heirs, but for yourself and your family right now.

What Are Living Benefits in Life Insurance?

Living benefits, often called “accelerated death benefits” or “riders,” are features built into or added to a life insurance policy that allow the policyholder to access a portion of their death benefit while still alive. This access typically triggers under specific circumstances, such as being diagnosed with a critical, chronic, or terminal illness. Instead of waiting for a death claim, these benefits provide a much-needed influx of cash to cover medical expenses, home modifications, lost income, or other significant costs that arise during a severe health event. This mechanism fundamentally shifts the utility of a life insurance policy. It moves beyond solely providing for beneficiaries after death, empowering the insured to utilize the policy’s value to navigate immense financial pressure during a health crisis. In an era where healthcare costs can be astronomically high, even with robust health insurance, living benefits offer a crucial layer of protection.

Why Living Benefits Matter in Today’s Financial Landscape (2026)

The year 2026 presents specific reasons why living benefits are more relevant than ever. Healthcare costs continue to outpace inflation, and the burden on individuals and families dealing with serious illness is immense. A 2023 report from the Kaiser Family Foundation, for instance, highlighted the persistent issue of high out-of-pocket costs, even for those with insurance, demonstrating a clear need for supplementary financial resources during health crises. Consider the practical implications:

- Mounting Medical Bills: Even with good health insurance, deductibles, co-pays, and non-covered services (like experimental treatments or extended home health care) can quickly deplete savings.

- Loss of Income: A serious illness often means an inability to work, either for the insured or a primary caregiver, leading to a significant drop in household income.

- Lifestyle Adjustments: Adapting homes for accessibility, specialized equipment, or travel for treatment can incur substantial, unexpected costs.

- Preserving Savings: Instead of draining retirement accounts or emergency funds, living benefits can act as a dedicated pool of funds for health-related emergencies, helping to maintain long-term financial stability. For many, understanding different types of insurance policies, whether for pets, cars, or life, is about mitigating risk across various aspects of life. Living benefits directly address the risk of catastrophic health expenses impacting one’s financial security while still living.

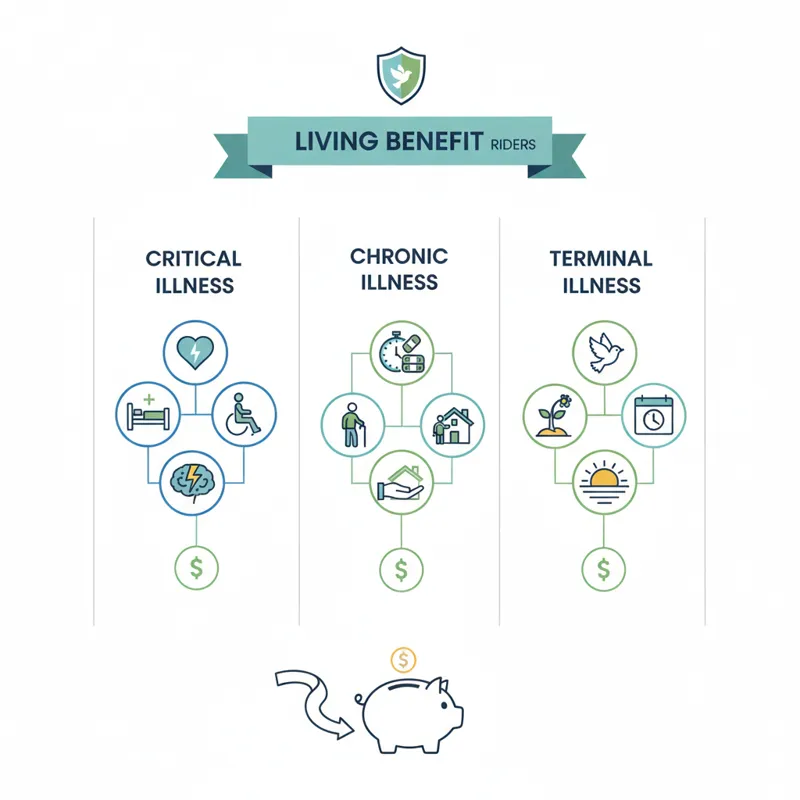

Core Types of Living Benefit Riders

While the specific names and triggers can vary by insurer and policy, most living benefits fall into a few primary categories. These are typically offered as riders, which are add-ons to a base life insurance policy, though some modern policies integrate them inherently.

1. Accelerated Death Benefit (ADB) for Terminal Illness

This is perhaps the most common and foundational living benefit. It allows the policyholder to access a significant portion (often up to 90-95%) of their death benefit if they are diagnosed with a terminal illness and have a life expectancy of 24 months or less, sometimes less depending on the policy. The primary purpose is to help cover end-of-life care, medical expenses, or even to fulfill a “bucket list” wish, providing comfort and financial relief during a difficult time. The amount received is typically subtracted from the policy’s face value, leaving a reduced death benefit for beneficiaries.

2. Chronic Illness Rider

A chronic illness rider provides access to a portion of the death benefit if the insured is unable to perform a certain number of Activities of Daily Living (ADLs) – typically two out of six – or suffers from severe cognitive impairment. ADLs include bathing, dressing, eating, toileting, transferring (moving from bed to chair), and continence. This benefit is designed to help cover costs associated with long-term care, such as home healthcare, assisted living facilities, or nursing home care. Unlike an ADB, a chronic illness diagnosis isn’t necessarily terminal, but it implies a prolonged need for care.

3. Critical Illness Rider

This rider allows access to a portion of the death benefit upon diagnosis of specific critical illnesses defined in the policy. Common critical illnesses include heart attack, stroke, cancer, kidney failure, major organ transplant, and paralysis. The payout from a critical illness rider is generally a lump sum, providing immediate funds to cover medical treatments, lost income during recovery, or even to pay off debts incurred during the illness. This differs from a chronic illness rider which is usually paid out in monthly installments to cover ongoing care.

4. Long-Term Care (LTC) Rider

While similar to a chronic illness rider, an LTC rider is specifically designed to function much like a standalone long-term care insurance policy, but as part of your life insurance. It often provides more comprehensive coverage for long-term care needs, including a wider range of services and potentially higher monthly benefits, with a defined benefit period. The trigger is also usually the inability to perform two or more ADLs or cognitive impairment. The funds from an LTC rider are typically paid out monthly to cover qualified long-term care expenses. Some policies offer a ‘hybrid’ approach, combining a life insurance death benefit with a robust long-term care component.

How Living Benefits Work: Practical Scenarios

To grasp the practical utility of life insurance with living benefits, consider these common scenarios:

- Scenario 1: Terminal Illness Diagnosis: Sarah, 55, is diagnosed with an aggressive cancer and given 12 months to live. Her traditional life insurance policy has an Accelerated Death Benefit rider. She chooses to accelerate 75% of her $500,000 death benefit, receiving $375,000. She uses these funds to pay for experimental treatments not fully covered by health insurance, make her home more comfortable, and cover her remaining mortgage payments so her family doesn’t have to worry about the house. Her beneficiaries will still receive the remaining $125,000 after her passing.

- Scenario 2: Chronic Illness Requiring Long-Term Care: Mark, 68, suffers a debilitating stroke that leaves him unable to dress or feed himself, requiring permanent assistance. His universal life insurance policy includes a Chronic Illness rider. Based on his inability to perform two ADLs, his policy allows him to access a monthly benefit for qualified long-term care expenses. This covers the cost of an in-home caregiver for several years, allowing him to stay in his own home instead of moving to a facility, preserving his savings and allowing his spouse to remain his partner, not just his caregiver.

- Scenario 3: Critical Illness Diagnosis: Maria, 42, is diagnosed with breast cancer. Her term life insurance policy has a Critical Illness rider. She receives a lump sum payout of $100,000, which she uses to cover her high deductible, co-pays for chemotherapy, and to take time off work for recovery without impacting her family’s income. This financial buffer allows her to focus on her health without the added stress of financial strain. These examples highlight how these benefits offer flexibility and financial relief precisely when it’s most needed.

Policy Types That Often Include Living Benefits

Living benefits aren’t exclusive to one type of life insurance. They can be found across various policy structures, though their availability and terms can differ.

Whole Life Insurance

Whole life policies are known for their guarantees, including a guaranteed death benefit, guaranteed cash value growth, and guaranteed premiums. Living benefits can be added as riders, making a stable, long-term policy even more robust. The cash value component of whole life policies can also be accessed through loans or withdrawals, providing another layer of liquidity, separate from living benefit riders.

Universal Life Insurance (UL, IUL, VUL)

Universal life policies offer more flexibility than whole life, allowing policyholders to adjust premiums and death benefits within certain limits.

- Traditional Universal Life (UL): Often includes living benefit riders, leveraging the cash value accumulation.

- Indexed Universal Life (IUL): These policies tie cash value growth to a stock market index, offering potential for higher returns while providing a floor against market losses. Many IUL policies are designed with robust living benefits as a core selling point, making them a popular choice for those seeking both growth potential and health security.

- Variable Universal Life (VUL): VUL policies allow policyholders to invest their cash value in sub-accounts, similar to mutual funds. While they offer higher growth potential, they also carry market risk. Living benefits can be added to VUL policies, providing a layer of protection against health crises irrespective of market performance.

Term Life Insurance with Living Benefit Riders

Historically, term life insurance was purely a death benefit product for a specific period. However, many insurers now offer term policies with accelerated death benefit riders for terminal illness, and some even include critical or chronic illness riders. This makes term life a more comprehensive option for those seeking temporary coverage with the added benefit of living protection, often at a more affordable premium than permanent policies.

What Most People Get Wrong About Living Benefits

Despite their clear advantages, several common misconceptions surround life insurance with living benefits. Clearing these up is crucial for informed decision-making.

They’re Not “Free Money”

A significant misunderstanding is that living benefits are an extra payout on top of the death benefit. In reality, any amount accessed through a living benefit rider is an acceleration of the death benefit. This means the amount paid out while you’re alive reduces the amount your beneficiaries will receive upon your death. It’s about re-prioritizing how the policy’s value is used – during your lifetime versus after.

Impact on Death Benefit and Policy Value

When you utilize a living benefit, it reduces the policy’s face amount. This reduction not only affects the death benefit paid to beneficiaries but can also impact the policy’s cash value, if it’s a permanent policy. For example, if you accelerate 50% of a $1 million policy, the death benefit becomes $500,000, and future cash value growth will be based on the reduced face amount.

Tax Implications Are Complex

While payouts for terminal and chronic illness are generally tax-free under current U. S. tax laws (IRS code sections 101(g) and 7702B), critical illness payouts might be subject to income tax depending on how they are structured and used. It’s always advisable to consult with a qualified tax advisor to understand the specific tax implications of receiving living benefits, especially since tax laws can change. This isn’t a “set it and forget it” tax situation.

Eligibility Nuances and Waiting Periods

Accessing living benefits isn’t automatic upon diagnosis. Policies have strict criteria:

- Medical Triggers: Specific definitions for critical, chronic, or terminal illnesses must be met. A diagnosis of cancer, for example, might not trigger a critical illness benefit if it’s an early stage and not considered “critical” by the policy’s definition.

- Life Expectancy: For terminal illness, a doctor’s certification of a limited life expectancy (e.g., 12 or 24 months) is required.

- ADL Requirements: For chronic illness, the inability to perform a specified number of ADLs must be certified by a licensed health care practitioner.

- Waiting Periods: Some riders may have waiting periods (e.g., 90 days after the policy is issued) before benefits can be claimed. Reading the fine print of your policy and understanding the exact triggers and limitations is absolutely critical. Just as you’d scrutinize the details of car insurance for a new vehicle, you need to understand the specifics of your life insurance riders.

Choosing the Right Policy: Key Considerations

Selecting the best life insurance with living benefits involves careful consideration of your personal circumstances and financial goals.

1. Your Health Status and Family History

Your current health and family medical history are significant. If there’s a history of certain critical or chronic illnesses in your family, prioritizing policies with robust critical or chronic illness riders might be prudent. Be honest and thorough during the application process to avoid issues later.

2. Financial Needs and Budget

Determine how much coverage you truly need. Consider your income, debts, dependents, and future financial obligations. Also, evaluate what you can comfortably afford in premiums. While comprehensive living benefits are appealing, they often come with an added cost, either built into the premium or as an explicit rider charge.

3. Policy Costs and Riders

Compare different insurers and policy types. Look beyond just the face value. Understand:

- Premium Structure: Is it level, increasing, or flexible?

- Rider Costs: Are riders included for free, or is there an additional charge?

- Benefit Payouts: What percentage of the death benefit can be accessed? Are there maximum annual or lifetime limits?

- Cash Value Growth: If considering permanent life insurance, how does the cash value grow, and how might using living benefits impact it?

4. Working with a Qualified Advisor

Navigating the complexities of living benefits can be challenging. A knowledgeable and independent financial or insurance advisor can help you:

- Assess your needs accurately.

- Compare policies from various carriers.

- Explain the nuances of different riders and their triggers.

- Ensure the policy aligns with your broader financial plan. A good advisor will educate you, not just sell you a product.

Navigating the Claims Process

When the need arises to file a claim for living benefits, the process typically involves:1. Notification: Inform your insurance company as soon as possible after a qualifying event (diagnosis, inability to perform ADLs).2. Documentation: The insurer will require medical documentation from your physician(s) confirming the diagnosis and meeting the policy’s criteria (e.g., terminal prognosis, specific critical illness, ADL assessment).3. Review: The insurance company reviews the submitted documentation against the policy’s specific terms and conditions for the rider in question.4. Payout: If approved, the benefit is paid out according to the policy’s terms—either a lump sum or monthly installments. It’s crucial to keep all medical records organized and communicate clearly with your healthcare providers about the need for specific documentation for your insurance claim. Having a clear understanding of your policy’s definitions beforehand can streamline this process.

The Future of Financial Security with Living Benefits

As we move further into 2026 and beyond, life insurance with living benefits is becoming less of a niche product and more of a standard expectation for comprehensive financial planning. It represents a forward-thinking approach to risk management, acknowledging that the financial burdens of severe illness can be as devastating as the emotional and physical ones. By providing access to funds during a health crisis, these policies empower individuals to make choices that prioritize their well-being and maintain their financial dignity, rather than being forced into difficult decisions due to lack of resources. They are a powerful tool for unlocking genuine financial security, offering protection not just for tomorrow, but for today. For those navigating the complexities of modern life, incorporating these benefits into your financial strategy isn’t just smart—it’s essential.

Frequently Asked Questions (FAQ) About Living Benefits

Can I get living benefits on an existing life insurance policy?

It depends on your policy and insurer. Some companies may allow you to add certain riders to an existing policy, but often, living benefits are integrated during the initial policy purchase. It’s best to contact your insurance agent or carrier to inquire about your specific policy’s options.

Are living benefits only for permanent life insurance?

No. While they are commonly associated with permanent policies like whole life and universal life, many term life insurance policies now offer accelerated death benefit riders for terminal illness, and some even include critical or chronic illness riders.

How much of my death benefit can I access through living benefits?

This varies significantly by policy and rider. For terminal illness riders, it’s often a substantial portion, like 50% to 95%. For critical or chronic illness riders, there might be annual or lifetime maximums, or it could be a smaller percentage of the total death benefit. Always check your policy’s specifics.

Are living benefits taxable?

Generally, payouts for terminal and chronic illnesses are tax-free under current U. S. tax laws. However, critical illness payouts may be taxable depending on the circumstances. It’s always crucial to consult a qualified tax advisor for personalized advice, as tax laws can change.

Do I have to pay back the money I receive from living benefits?

No, you do not “pay back” the money. When you utilize a living benefit, you are essentially accelerating a portion of your death benefit. This amount is permanently deducted from the policy’s face value, and the remaining amount is what your beneficiaries will receive upon your passing.

What happens if I don’t use my living benefits?

If you never meet the criteria to trigger a living benefit, or simply choose not to use it, your life insurance policy will pay out its full death benefit (minus any policy loans or outstanding charges) to your beneficiaries upon your death, just like a traditional policy.

Disclaimer: This article provides general information and understanding of life insurance with living benefits. It is not intended as financial, legal, or medical advice. Insurance products and regulations vary, and individual circumstances differ. Always consult with a qualified insurance professional, financial advisor, tax professional, and healthcare provider to discuss your specific situation and make informed decisions.