Navigating the landscape of pet care in Florida requires a proactive approach, especially when considering the unexpected. As any pet owner knows, our furry companions are integral family members, bringing immense joy and companionship. Yet, their health, much like our own, can present unforeseen challenges and significant veterinary costs. This is where pet insurance in Florida steps in, offering a crucial safety net against the financial strain of accidents, illnesses, and even routine wellness needs. In 2026, with veterinary medicine continuously advancing and the cost of care steadily climbing, understanding and selecting the right pet insurance plan isn’t just a luxury—it’s becoming an essential component of responsible pet ownership. This guide will walk you through the mechanics, types of coverage, cost factors, and specific considerations for Florida pet owners, helping you make an informed decision to protect your beloved animal.

Understanding the Unique Needs for Pet Insurance in Florida

Florida presents a distinct set of environmental and health challenges for pets that make robust insurance coverage particularly valuable. Our warm climate, while enjoyable, contributes to a longer and more intense season for parasites like fleas, ticks, and mosquitoes, increasing the risk of heartworm disease, Lyme disease, and other vector-borne illnesses. Furthermore, the state’s abundant wildlife, from snakes and alligators to raccoons and various insects, means encounters requiring emergency veterinary intervention are not uncommon.

Beyond these specific risks, the general cost of living and specialized veterinary care in many parts of Florida can be substantial. An unexpected emergency, such as a fractured bone from an accident, a sudden illness like pancreatitis, or a chronic condition requiring ongoing management, can quickly lead to bills running into thousands of dollars. Having solid pet insurance Florida coverage helps mitigate these financial shocks, ensuring you can prioritize your pet’s health without the added burden of prohibitive costs.

How Pet Insurance Works: The Fundamental Mechanics

At its core, pet insurance operates similarly to human health insurance, albeit with a common reimbursement model. You pay a monthly or annual premium to an insurance provider. When your pet needs veterinary care for a covered condition, you pay the vet directly, then submit a claim to your insurer for reimbursement.

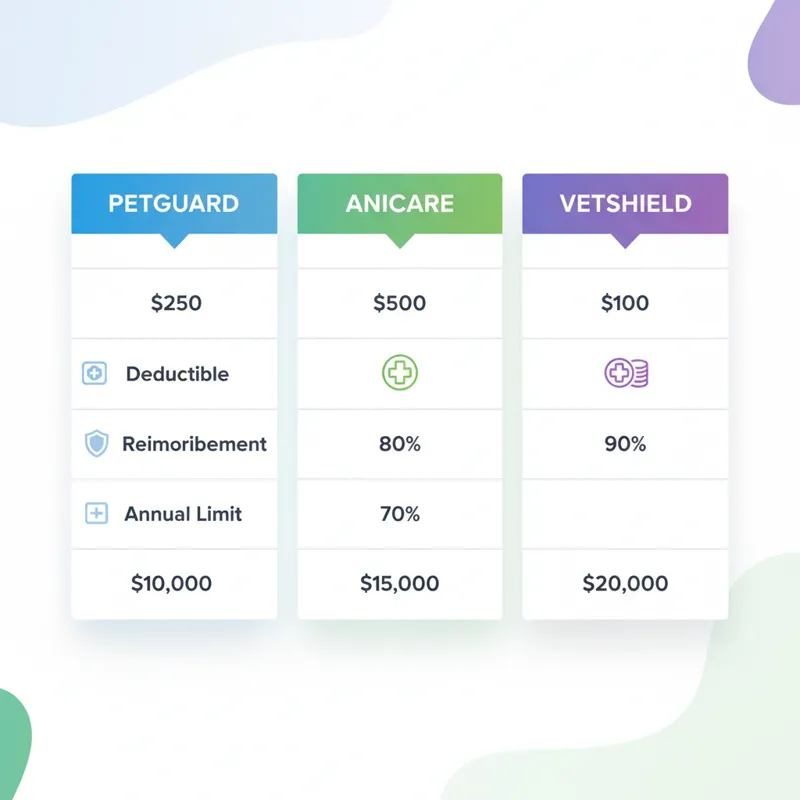

- Deductible: This is the amount you must pay out-of-pocket before your insurance company starts reimbursing you. Deductibles are typically annual, meaning once met, the insurer will contribute to covered expenses for the remainder of that policy year. Common deductible amounts range from $100 to $1,000.

- Reimbursement Percentage: After meeting your deductible, this is the percentage of the remaining vet bill that the insurance company will cover. Common reimbursement percentages are 70%, 80%, or 90%. If your vet bill is $1,000, your deductible is $250, and your reimbursement is 80%, you’d pay the $250 deductible, and the insurer would cover 80% of the remaining $750 ($600), leaving you to pay $150.

- Annual Limit: This is the maximum amount your insurance company will pay out in a policy year. Limits can range from $2,500 to unlimited. Choosing a higher annual limit often means a higher premium, but provides greater peace of mind for very expensive incidents.

Understanding these three components is key to grasping how any pet health plan will function financially. They are adjustable parameters that directly influence your monthly premium and your out-of-pocket costs when a claim arises.

Understanding the Spectrum of Pet Insurance Plans

Pet insurance isn’t a one-size-fits-all solution. Providers typically offer several plan types, each designed to cover different levels of care. The most common options include accident-only, accident and illness, and wellness add-ons.

Disclaimer: This article provides general information and is not financial advice. Readers should consult with licensed insurance professionals or veterinarians to make informed decisions tailored to their specific circumstances.

Accident-Only Plans

These plans are the most basic and typically the most affordable. They cover costs associated with unexpected injuries, such as broken bones, swallowed objects, car accidents, snake bites, or cuts and lacerations. They do not cover illnesses, chronic conditions, or routine care. An accident-only plan can be a good choice for younger, healthier pets or for owners seeking a budget-friendly option to protect against sudden, high-cost emergencies.

Accident & Illness Plans (Comprehensive Coverage)

This is the most popular type of pet insurance in Florida, offering a broader range of coverage. Beyond accidents, these plans cover illnesses ranging from minor conditions like ear infections to major ones like cancer, diabetes, arthritis, and allergies. They often include coverage for diagnostics (X-rays, blood tests), hospitalization, surgery, prescription medications, and emergency care. Most comprehensive plans exclude pre-existing conditions (more on this later) and routine preventative care unless a specific rider is added.

Wellness Plans or Routine Care Add-ons

Wellness plans are generally not standalone insurance policies but rather optional riders or separate packages designed to cover preventative care. This includes vaccinations, annual check-ups, heartworm prevention, flea and tick control, and sometimes spaying or neutering. While these plans help spread out the cost of routine care, they don’t cover unexpected accidents or illnesses. For many, integrating a wellness plan with an accident & illness policy offers the most comprehensive approach to pet health management.

Navigating the array of pet insurance options can feel as specialized as understanding the nuances of ultimate tips for perfect vanilla chai tea, each blend offering a different experience. Similarly, each plan type provides distinct benefits and limitations.

Key Factors Influencing Your Pet Insurance Florida Premium

The cost of pet coverage in Florida varies significantly based on several key factors. Understanding these elements can help you anticipate expenses and make informed choices when comparing pet insurance providers Florida.

Pet’s Age, Breed, and Species

- Age: Younger pets are cheaper to insure because they are less likely to have existing conditions or develop new ones. Premiums generally increase as your pet ages.

- Breed: Certain breeds are predisposed to specific genetic or hereditary conditions. For instance, large breeds might be prone to hip dysplasia, while some purebreds are known for cardiac issues. Insurers factor these risks into the premium.

- Species: Dogs are generally more expensive to insure than cats, primarily due to their larger size (meaning higher medication dosages, surgical costs) and typically higher incidence of certain conditions. Exotic pets often have very limited or no coverage options.

Your Location Within Florida

Veterinary costs can differ significantly depending on where you live in Florida. Major metropolitan areas like Miami, Orlando, or Tampa typically have higher vet fees due to higher operating costs, specialized equipment, and greater demand. This regional variation directly impacts your pet insurance Florida premium.

Deductible, Reimbursement, and Annual Limit Choices

These are the primary levers you can pull to adjust your premium:

- Higher Deductible: Choosing a higher deductible lowers your monthly premium but means you pay more out-of-pocket before coverage kicks in.

- Lower Reimbursement Percentage: Opting for 70% reimbursement instead of 90% reduces your premium, but you bear a larger portion of the covered vet bill.

- Lower Annual Limit: Selecting a lower annual limit (e.g., $5,000 instead of unlimited) makes your premium cheaper but caps the total amount the insurer will pay in a year.

Pre-existing Conditions

This is one of the most critical aspects of pet insurance. Virtually all pet insurance policies exclude pre-existing conditions, meaning any illness or injury that showed symptoms or was diagnosed before your policy’s start date or during its waiting periods. Some providers differentiate between ‘curable’ and ‘incurable’ pre-existing conditions, offering potential coverage for curable conditions (e.g., a one-time ear infection) after a specific symptom-free period. It’s crucial to enroll your pet when they are young and healthy to avoid future exclusions.

Just as selecting the best porcelain tea set designs for your home involves considering aesthetics and functionality, choosing the right pet insurance plan requires a similar level of thoughtful comparison, particularly regarding what it will and won’t cover.

Comparing Top Pet Insurance Providers in Florida: What to Look For

When you compare pet insurance providers Florida, you’ll encounter a range of companies, each with slightly different offerings. While we won’t endorse specific providers here, understanding the general criteria for evaluation is key.

- Reputation and Customer Service: Research reviews regarding claim processing speed, customer support responsiveness, and overall satisfaction.

- Policy Flexibility: Can you customize your deductible, reimbursement percentage, and annual limit to fit your budget and needs?

- Transparency: Are the terms and conditions clear? Are exclusions plainly stated? A good provider makes it easy to understand what you’re buying.

- Waiting Periods: Pay close attention to these. They can vary significantly for accidents (often a few days) and illnesses (typically 14-30 days). Some have longer waiting periods for orthopedic conditions.

- Coverage Details: What exactly is covered under “illness” or “accident”? Are things like behavioral therapy, alternative therapies, or prescription food included?

- Direct Vet Pay: While most operate on a reimbursement model, a few providers offer direct payment to vets, which can be a significant benefit if you’re not in a position to pay large upfront sums.

Many providers offer instant online quotes, making it straightforward to compare costs and coverage for your specific pet in Florida. Don’t shy away from getting multiple quotes to find the best fit.

Is Pet Insurance Worth It in Florida? A Practical Cost-Benefit Analysis

The question, “Is pet insurance worth it Florida?” is a common one, and the answer often depends on your financial situation, your pet’s health, and your risk tolerance. Let’s look at it practically.

The Scenario of High-Cost Emergencies

Consider common Florida scenarios:

- Snake Bite: Treatment can range from $1,500 to $10,000+, depending on the snake, severity, and required antivenom.

- Accidental Ingestion: If your dog eats something toxic (e.g., rat poison, chocolate), emergency vet visits, induced vomiting, hospitalization, and supportive care can easily run $500 to $3,000.

- Chronic Illness: A diagnosis of diabetes, kidney disease, or cancer can lead to ongoing costs for medication, specialized food, and regular vet visits that easily exceed $1,000-$2,000 per year, for the pet’s remaining life.

Without pet insurance, you are solely responsible for these costs. For many families, an unexpected $5,000 vet bill can be a significant financial strain, potentially forcing difficult decisions about a beloved pet’s care.

Potential Savings and Peace of Mind

With an average monthly premium of $40-$70 for a dog (and less for a cat), annual costs might be $480-$840. In a high-cost scenario like a $5,000 emergency with an 80% reimbursement and $250 deductible, you would pay your $250 deductible + 20% of the remaining $4,750 ($950), for a total out-of-pocket of $1,200 (plus your premiums). The insurance would save you $3,800. For ongoing chronic conditions, the savings compound over years.

Beyond the financial calculation, there’s the invaluable peace of mind. Knowing you won’t have to choose between your pet’s life and your financial stability is a powerful motivator for many. It allows you to focus on your pet’s recovery rather than scrambling for funds.

Alternative: The Emergency Fund

Some people opt to self-insure by maintaining a dedicated pet emergency fund. This can be a viable strategy if you’re disciplined and can consistently set aside a substantial amount (e.g., $5,000-$10,000). The drawback is that emergencies can happen before you’ve built up a sufficient fund, or a single major event could deplete it entirely. Pet insurance, in contrast, offers immediate large-scale financial protection from day one (after waiting periods).

Things People Usually Miss About Pet Insurance Florida

While the basic mechanics are straightforward, several nuances often catch pet owners off guard. Being aware of these details can prevent future disappointments.

- Waiting Periods Aren’t Just for Illness: While illness waiting periods are common (usually 14 days), many policies also have a waiting period for accidents (often 2-3 days). Some specific conditions, like hip dysplasia or cruciate ligament issues, may have even longer waiting periods (e.g., 6-12 months), even if not present at enrollment. Always check these specifics.

- Bilateral Conditions: This is critical for breeds prone to certain issues. If your pet develops a condition on one side of their body (e.g., a luxating patella in one knee) before coverage or during a waiting period, and later develops the same condition on the other side, the second occurrence might be considered a pre-existing condition and thus excluded.

- Mandatory Vet Exam: Most insurers require a full veterinary exam within a certain timeframe (e.g., 12 months) prior to or shortly after enrollment. This helps them establish a baseline of your pet’s health and identify any pre-existing conditions. Failing to provide this can invalidate claims.

- Inflation and Escalating Vet Costs: While your policy helps, vet costs consistently rise. Your deductible and reimbursement percentage remain fixed, but the actual dollar amounts you pay out-of-pocket will naturally increase with the cost of treatment. Some policies offer options to adjust coverage annually, but it’s not automatic inflation protection.

- Understanding Policy Riders: Wellness plans are common riders, but so are options for behavioral therapy, prescription food, or even end-of-life care. These add-ons significantly increase premiums, so evaluate if the benefits truly align with your specific needs.

- The Reimbursement Model is Standard: Don’t expect to walk out of the vet without paying. You’ll almost always pay the vet bill in full first and then wait for the insurer to reimburse you. Ensure you have the immediate funds available, or discuss payment options with your vet beforehand.

Florida-Specific Considerations for Pet Owners

Living in the Sunshine State brings unique environmental factors that directly impact pet health and, by extension, the utility of pet insurance.

- Heat-Related Illnesses: Florida’s intense heat and humidity pose a constant risk of heatstroke, especially for brachycephalic (short-nosed) breeds like bulldogs and pugs. Treatments can involve IV fluids, cooling measures, and organ support, leading to significant costs.

- Parasite Control: Year-round warmth means year-round flea, tick, and mosquito activity. Heartworm disease is endemic, and other tick-borne diseases are prevalent. While preventative medications are often part of wellness plans, treating established infections or diseases like heartworm can be expensive and complex. Florida Department of Health provides resources on zoonotic diseases, highlighting the importance of preventative care often covered by wellness plans.

- Wildlife Encounters: Snake bites (venomous and non-venomous), alligator attacks, and encounters with other wildlife are genuine risks. Immediate veterinary care is crucial and can involve emergency surgery, antivenom, antibiotics, and extensive hospitalization.

- Toxic Plants and Algae: Florida’s diverse flora includes many plants toxic to pets. Additionally, harmful algal blooms can occur in freshwater bodies, posing a severe threat if ingested. Rapid emergency intervention is often necessary.

- Hurricane Preparedness: While not a direct health risk, hurricane season can disrupt access to veterinary care or lead to stress-related illnesses in pets. Having pet insurance helps cover unexpected issues that might arise during such stressful periods. The ASPCA offers extensive guides on preparing pets for natural disasters, a crucial consideration for any Florida resident.

These local specificities emphasize why comprehensive pet insurance in Florida isn’t just a good idea, but a practical necessity for many.

The diverse array of pet health plans available today rivals the variety you might find exploring ultimate tea varieties in Spanish-speaking cultures, each with its own unique characteristics and benefits.

How to Choose the Best Pet Insurance Plan for Your Needs

Selecting the right pet insurance Florida plan involves a thoughtful process tailored to your unique circumstances and your pet’s specific requirements.

- Assess Your Pet’s Risks: Consider your pet’s breed, age, and general health. A young, healthy mixed-breed might do well with a standard accident & illness plan, while an older purebred with known breed-specific predispositions might benefit from higher limits and a plan known for good coverage of chronic conditions.

- Evaluate Your Budget and Risk Tolerance: Determine how much you’re comfortable paying monthly for premiums versus how much you’re willing to pay out-of-pocket for vet bills. Can you comfortably afford a $1,000 deductible, or would a $250 deductible, despite higher premiums, provide more financial security?

- Read Sample Policies Carefully: Don’t just look at quotes. Request and review a sample policy from any insurer you’re seriously considering. Pay close attention to the fine print, especially regarding exclusions, waiting periods, and how pre-existing conditions are defined and handled.

- Get Multiple Quotes and Compare: Use online comparison tools or directly contact several providers. Compare not just the premium, but also the deductible, reimbursement percentage, annual limits, and what’s covered or excluded. Forbes Advisor frequently reviews and compares pet insurance providers, which can be a valuable starting point for research.

- Consider Future Costs: Remember that premiums typically increase with your pet’s age. While you can’t predict exact future costs, factor in the long-term commitment.

- Consult Your Veterinarian: Your vet often has insights into common local health issues and can provide guidance on what kind of coverage might be most beneficial for your pet’s breed and lifestyle. They also know which insurance companies process claims efficiently.

Frequently Asked Questions (FAQ) About Pet Insurance Florida

Does pet insurance cover pre-existing conditions?

Generally, no. Most policies exclude conditions that were symptomatic or diagnosed before the policy start date or during a waiting period. Some insurers might cover ‘curable’ conditions after a period free of symptoms, but this varies. Enrolling a pet when young and healthy is crucial to maximize coverage.

Can I use any veterinarian with pet insurance?

Yes, typically. Most pet insurance policies operate on a reimbursement model, meaning you pay your vet directly, then submit the bill to your insurer. This allows you the flexibility to visit any licensed veterinarian, specialist, or emergency clinic you choose, without network restrictions.

What’s the typical cost of pet insurance in Florida?

The cost varies widely based on your pet’s species, age, breed, location, and the specifics of your chosen plan (deductible, reimbursement, annual limit). For a dog in Florida, expect to pay anywhere from $40 to $70 per month for comprehensive accident & illness coverage. Cats are generally less, often $20-$40 per month.

When is the best time to get pet insurance?

The best time to enroll your pet is when they are young and healthy. This ensures you avoid exclusions for pre-existing conditions and secure the lowest possible premiums, which will gradually increase with age but will generally remain lower than if you started a policy later in life.

Does pet insurance cover routine wellness exams or vaccinations?

Only if you opt for a separate wellness plan or add a wellness rider to your accident & illness policy. Standard accident & illness plans focus solely on unexpected medical events and do not cover routine preventative care.

Conclusion

The decision to invest in pet insurance in Florida is a personal one, but it’s a choice rooted in practicality and foresight. Given Florida’s unique environmental challenges and the ever-increasing costs of veterinary care, comprehensive coverage offers a robust defense against financial hardship and ensures your pet receives the best possible care when they need it most. By understanding the different plan types, recognizing the factors that influence premiums, and diligently comparing providers, you can confidently select a pet insurance plan that provides invaluable peace of mind and protection for your cherished companion for years to come. Don’t wait for an emergency to realize the profound value of being prepared.

General Information & Professional Disclaimer

Disclaimer

The information provided by bangladeshcountry.com (“we,” “us,” or “our”) on our website is for general informational purposes only. All information on the Site is provided in good faith; however, we make no representation or warranty of any kind, express or implied, regarding the accuracy, adequacy, validity, reliability, availability, or completeness of any information on the Site.

Not Professional Advice The Site cannot and does not contain financial, insurance, legal, medical or professional career advice. The insurance related information is provided for general informational purposes only and is not a substitute for professional advice.

We are not certified financial advisors, insurance agents, or legal professionals. Accordingly, before taking any actions based on such information, we strictly encourage you to consult with the appropriate professionals or certified authorities. We do not provide any kind of professional or financial advice.

THE USE OR RELIANCE OF ANY INFORMATION CONTAINED ON THIS SITE IS SOLELY AT YOUR OWN RISK. We shall not have any liability to you for any loss or damage of any kind incurred as a result of the use of the site or reliance on any information provided on the site.