Riding a motorcycle in Florida offers a unique sense of freedom, with endless miles of scenic routes and year-round sunshine. But before you hit the open road, a critical question often arises: do you really need motorcycle insurance in Florida? It’s a common point of confusion, largely because Florida’s insurance landscape, especially concerning two-wheeled vehicles, operates differently from many other states. While car owners are familiar with the state’s no-fault PIP requirements, motorcycles are carved out of this system, leading to misunderstandings about what’s legally required and, perhaps more importantly, what’s financially essential. This isn’t just about following the law; it’s about understanding the real-world implications for your finances and well-being should an accident occur.

The Short Answer: Is Motorcycle Insurance Required in Florida?

Here’s where things get interesting and often misunderstood: unlike passenger vehicles, Florida law does not mandate that motorcyclists carry Personal Injury Protection (PIP) coverage. This is a direct exemption from the state’s no-fault statute that applies to cars. So, if you’re asking if you need to have a policy in hand before you can legally ride your motorcycle, the answer isn’t a simple ‘yes’ or ‘no’ like it is for a car. It’s more nuanced.

Florida operates under a Financial Responsibility Law for motorcycles. This law essentially states that if you are involved in an accident that causes bodily injury or property damage, you must be able to prove financial responsibility at the time of the crash. If you can’t, you face severe penalties, including license and registration suspension. While insurance isn’t explicitly required to get your tag, it’s the most common and practical way to satisfy this contingent financial responsibility.

Therefore, while you might technically register your motorcycle without an active insurance policy, choosing to ride without one means you’re taking on significant personal financial risk. The law essentially waits for an incident to occur before it demands proof of your ability to pay. It’s a reactive system rather than a proactive one for upfront coverage.

Why Florida’s Motorcycle Insurance Laws Are Different

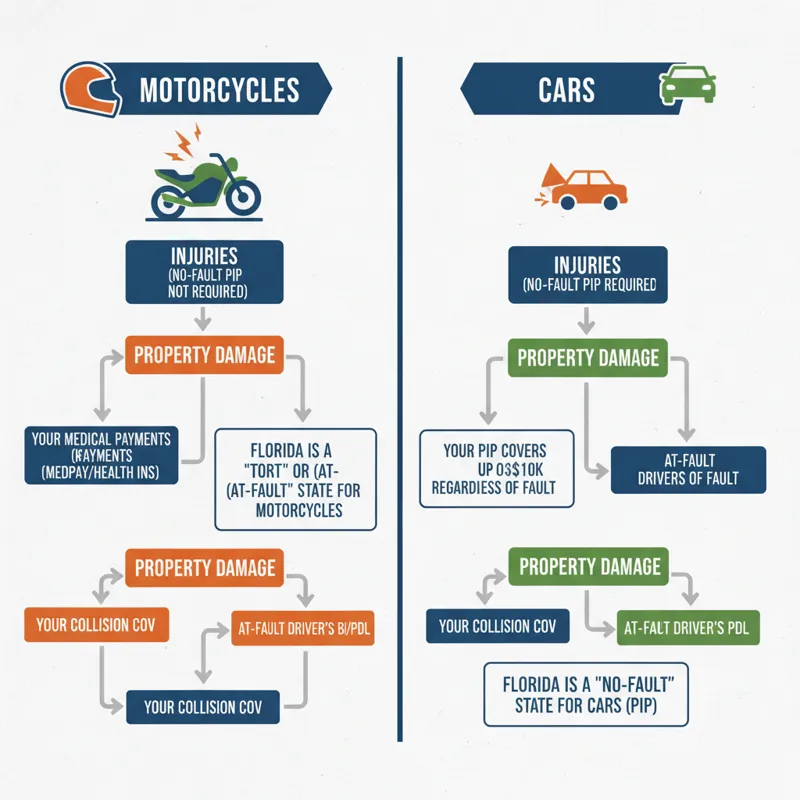

To fully grasp the situation, we need to understand Florida’s broader insurance framework. For cars, Florida is a “no-fault” state. This means that after a car accident, your own PIP coverage pays for your medical expenses and lost wages, regardless of who caused the crash. It’s designed to streamline minor accident claims and reduce litigation.

Motorcycles, however, are explicitly excluded from this no-fault system by Florida Statute. This exclusion has profound implications. First, it means motorcyclists are not required to carry PIP. Second, and crucially, it means motorcyclists operate under a traditional “at-fault” system when it comes to liability for bodily injury and property damage. If you cause an accident on your motorcycle, you are personally liable for the damages and injuries of others, and vice-versa.

This distinction is critical. Without PIP, if you’re injured in a motorcycle accident, your own medical bills won’t automatically be covered by a basic state-mandated policy like they would be if you were in a car. You’d need other forms of health coverage or specific motorcycle medical payments coverage. The financial responsibility law then steps in to ensure that if you’re the at-fault party, you can pay for the damages you caused to others.

The state’s approach essentially puts the onus on the rider to decide how to manage risk, knowing that if an accident occurs, the full financial weight of liability (and personal injury) rests squarely on them.

Decoding Florida’s Financial Responsibility Law for Motorcyclists

Florida Statute Chapter 324, often referred to as the Financial Responsibility Law, is the key legislation for motorcyclists in the state. While it doesn’t mandate upfront insurance purchase, it does set clear expectations for financial accountability if an incident occurs. Specifically, if you’re involved in an accident that results in injury, death, or significant property damage, you must prove you had the ability to cover the minimum liability requirements at the time of the crash.

What are these minimum requirements? The law typically specifies coverage limits for bodily injury liability (BIL) and property damage liability (PDL). As of 2026, these are generally:

- $10,000 for bodily injury or death of one person.

- $20,000 for bodily injury or death of two or more persons.

- $10,000 for property damage liability.

This is often expressed as 10/20/10 coverage.

Failing to demonstrate this financial responsibility can lead to severe consequences. The Florida Department of Highway Safety and Motor Vehicles (FLHSMV) can suspend your driver’s license, motorcycle endorsement, and vehicle registration until you provide proof of financial responsibility and maintain it for three years. This proof usually takes the form of an SR-22 certificate from an insurance company, indicating future financial responsibility. Imagine losing your riding privileges for years, alongside potential lawsuits and personal financial ruin. This legal framework makes proactively obtaining insurance the most sensible and common approach for almost every rider.

For more detailed information on Florida’s motor vehicle laws, including specific statutes, you can refer to the Florida Department of Highway Safety and Motor Vehicles website.

The Risks of Riding Uninsured in Florida (Beyond the Law)

While understanding the legal nuances of Florida’s Financial Responsibility Law is important, the practical and financial risks of riding without motorcycle insurance extend far beyond potential legal penalties. These are the risks that can truly devastate your life savings and future.

Personal Injury Costs

Even if you’re an exceptionally careful rider, accidents happen. When they do, medical bills can quickly skyrocket. Without PIP, as discussed, you’re on your own. A single emergency room visit, ambulance ride, surgery, or prolonged rehabilitation can easily cost tens of thousands, or even hundreds of thousands of dollars. Your standard health insurance might cover some of this, but often with high deductibles, co-pays, and limits that motorcycle-related injuries can quickly exceed. The physical pain is enough; adding crippling debt makes it exponentially worse.

Property Damage Liability

If you’re at fault in an accident, you’re responsible for the damage to other vehicles or property. Imagine T-boning a new luxury SUV or colliding with a storefront. Repairing or replacing these items can cost thousands. If you don’t have property damage liability coverage, that bill comes directly to you. Your assets, like your home, savings, or future earnings, could be at risk.

Bodily Injury Liability

This is arguably the most significant financial risk. If you injure another person in an accident you cause, they can sue you for their medical expenses, lost wages, pain and suffering, and more. Settlements or court judgments can easily reach hundreds of thousands, or even millions, of dollars. Without adequate bodily injury liability insurance, you could face legal judgments that wipe out your entire financial net worth, force you into bankruptcy, and garnish your wages for years to come.

Uninsured/Underinsured Motorist Situations

What if someone else hits you, and they don’t have enough insurance (or any at all) to cover your injuries and damages? Florida has a significant number of uninsured drivers. If you don’t have Uninsured/Underinsured Motorist (UM/UIM) coverage on your own policy, you might be left with no recourse to cover your medical bills, lost income, and bike repairs, even if you weren’t at fault. This type of insurance protects you from financially irresponsible drivers.

Considering these potential scenarios, the decision to ride uninsured shifts from a question of legal requirement to one of fundamental personal financial protection. It’s a gamble with potentially life-altering stakes.

Essential Types of Motorcycle Coverage You Should Consider in Florida

Given the risks, proactively securing a robust motorcycle insurance policy in Florida is not just a good idea—it’s a prudent financial necessity. Here’s a breakdown of the essential types of coverage you should consider, moving beyond the bare minimum and focusing on comprehensive protection:

Bodily Injury Liability (BIL)

This coverage pays for medical expenses, lost wages, and pain and suffering for others if you are at fault in an accident. Florida’s Financial Responsibility Law mandates minimum limits if an accident occurs, but these minimums (10/20) are often woefully inadequate in a serious accident. Carrying higher limits, like $50,000/$100,000 or even $100,000/$300,000, provides a much stronger shield against personal lawsuits and financial ruin. This is your primary defense against catastrophic liability claims.

Property Damage Liability (PDL)

Similar to BIL, PDL pays for damage you cause to another person’s property, such as their vehicle, motorcycle, fence, or even a building, if you are found at fault. The state minimum ($10,000) for property damage might not even cover a minor fender bender with an expensive vehicle today. Opting for higher limits, such as $25,000 or $50,000, offers significantly better protection.

Uninsured/Underinsured Motorist (UM/UIM)

This coverage is critical in Florida due to the high number of uninsured drivers. UM/UIM protects you and your passengers if you are injured by a driver who has no insurance (uninsured) or not enough insurance (underinsured) to cover your damages. It can cover your medical bills, lost wages, and pain and suffering. It’s an often-overlooked but incredibly valuable part of any comprehensive protection plan.

Medical Payments (MedPay)

Since motorcycles are exempt from Florida’s PIP requirements, MedPay is your primary go-to for immediate medical expenses, regardless of fault. It covers reasonable medical, surgical, dental, and funeral expenses for you and your passengers if injured in an accident. The coverage limits are typically lower than health insurance but activate quickly and can cover deductibles or co-pays from your primary health plan. It’s a vital layer of protection for your own well-being.

Collision Coverage

This coverage pays for damages to your motorcycle if it collides with another vehicle or object, regardless of who is at fault. It’s essential for protecting your investment in your bike. If you have a loan on your motorcycle, your lender will almost certainly require you to carry collision coverage.

Comprehensive Coverage

Comprehensive coverage protects your motorcycle from non-collision events. This includes theft, vandalism, fire, natural disasters (like hurricanes, common in Florida!), and impacts with animals. Like collision, it’s typically required by lenders and is crucial for protecting your bike when it’s not on the road or involved in a crash.

Accessory Coverage

Many riders invest heavily in custom parts, chrome, fairings, saddlebags, and other accessories. Standard collision and comprehensive policies often have limited coverage for these extras. Accessory coverage allows you to insure your customizations up to a higher specified limit, ensuring your unique modifications are protected.

When you get a policy quote, consider these types of insurance. Each component offers a specific layer of protection, building a comprehensive safety net for your riding experience in Florida.

What Most People Get Wrong About Florida Motorcycle Insurance

The unique nature of Florida’s motorcycle laws leads to several widespread misconceptions. Understanding these can prevent costly errors and ensure you’re adequately protected.

“I Don’t Need Insurance Because Florida is a No-Fault State.”

This is perhaps the biggest and most dangerous misconception. While Florida is a no-fault state for cars, motorcycles are explicitly excluded from the PIP requirement. This means two critical things:

- You are not automatically covered for your own medical expenses by a no-fault system.

- If you are at fault in an accident, you are fully liable for damages and injuries to others, operating under traditional at-fault tort law.

Riding uninsured based on this misunderstanding is a direct path to financial catastrophe.

“My Health Insurance Will Cover Everything if I Get Hurt.”

While your health insurance will certainly help, it’s not designed to handle the specific aftermath of an accident, particularly involving a motorcycle. Health insurance typically doesn’t cover lost wages, extended rehabilitation that falls outside specific medical treatments, or the pain and suffering component of an injury. It also won’t cover your deductible, nor will it cover damages to your bike. Medical Payments (MedPay) through your motorcycle insurance fills crucial gaps and kicks in faster for accident-related care.

“I Only Need Insurance if I Have a Loan on My Bike.”

While lenders do require comprehensive and collision coverage to protect their investment, the need for insurance goes far beyond satisfying a loan. The liability risks – for bodily injury and property damage you cause to others – exist whether your bike is paid off or not. Your personal assets are on the line regardless of your loan status.

“Motorcycle Insurance is Too Expensive, So I’ll Just Take My Chances.”

While premiums vary, the cost of even basic liability coverage pales in comparison to the potential financial fallout of a single accident. The decision to forgo insurance to save a few hundred dollars a year could lead to hundreds of thousands in debt or a lifetime of financial struggle. Smart shoppers compare protection plans and look for affordable coverage options, knowing it’s an investment in peace of mind.

“The State Doesn’t Require Me to Have Insurance to Register My Bike, So It Must Not Be That Important.”

This misunderstanding conflates upfront registration requirements with post-accident financial responsibility. Florida’s law is reactive: it demands proof of financial responsibility after an accident. By then, it’s too late. The lack of an upfront mandate doesn’t diminish the critical importance of being proactively insured. Understanding deductibles and limits on your chosen policy will help you manage costs without sacrificing essential coverage.

How to Get a Motorcycle Insurance Policy Quote in Florida

Securing a motorcycle insurance policy in Florida involves several steps and considerations to ensure you get the right coverage at a competitive price. It’s not just about finding the cheapest option, but the best value that offers robust protection.

Factors Influencing Your Premium

Several variables impact your insurance costs:

- Your Riding History: A clean driving record with no accidents or tickets will generally yield lower premiums.

- Your Age and Experience: Younger, less experienced riders often face higher rates.

- Type of Motorcycle: Sport bikes, high-performance models, and expensive custom bikes typically cost more to insure due to higher repair costs and increased risk profiles. Cruisers and touring bikes might be more affordable.

- Location: Where you live and park your motorcycle in Florida can affect rates, especially in areas with higher theft rates or traffic density.

- Coverage Limits and Deductibles: Higher liability limits mean higher premiums, but also better protection. Higher deductibles on comprehensive and collision coverage can lower your premium, but mean you pay more out-of-pocket after a claim.

- Credit Score: In many states, including Florida, your credit-based insurance score can influence your premium, as it’s statistically linked to claim likelihood.

- Discounts: Many leading providers offer discounts for rider safety courses, multi-policy bundling (e.g., car and motorcycle insurance with the same company), motorcycle club memberships, anti-theft devices, and paying your premium in full.

Tips for Finding Affordable Coverage Options

Don’t just settle for the first quote you receive. Here’s how to find competitive rates:

- Shop Around: Get quotes from multiple insurance companies. Different providers have different underwriting criteria and may offer varying rates for the same coverage. This is crucial for comparing protection plans.

- Enroll in a Rider Safety Course: Completing an approved motorcycle safety course (like those offered by the Motorcycle Safety Foundation) can not only make you a safer rider but also qualify you for discounts.

- Bundle Policies: If you have car insurance, home insurance, or renters insurance, check if your current provider offers a discount for bundling your motorcycle policy.

- Review Coverage Annually: Your needs and the market can change. Review your policy at least once a year to ensure you still have the best rates and appropriate coverage for your current situation.

When you get a policy quote, clearly understand what’s included. Don’t hesitate to ask questions about understanding deductibles, coverage limits, and any exclusions. Look into leading providers known for their motorcycle insurance offerings, as they often have specialized policies tailored to riders’ needs.

Frequently Asked Questions (FAQ) About Florida Motorcycle Insurance

Is it true that I don’t need a helmet in Florida, and how does that affect insurance?

Florida law states that riders 21 and older are not required to wear a helmet if they have an insurance policy that provides at least $10,000 in medical benefits for injuries incurred in a motorcycle accident. This medical benefits coverage is not PIP, but typically comes from Medical Payments (MedPay) or specific add-on coverage within a motorcycle policy. So, while you technically can ride without a helmet if you meet this insurance criterion, it’s a separate legal requirement, and carrying appropriate medical coverage is the key to that exception. Many riders still choose to wear a helmet for safety, regardless of the law.

Can my car insurance policy extend to cover my motorcycle?

Generally, no. Your standard car insurance policy is specifically designed for automobiles and their associated risks. Motorcycles have different risk profiles, repair costs, and liability considerations. You will need a separate, dedicated motorcycle insurance policy to cover your bike and riding risks.

What exactly is a deductible in motorcycle insurance?

A deductible is the amount of money you agree to pay out-of-pocket for a claim before your insurance coverage kicks in. For example, if you have a $500 deductible for collision coverage and your bike sustains $2,000 in damage, you’d pay the first $500, and your insurance company would pay the remaining $1,500. Choosing a higher deductible often lowers your monthly or annual premium, but means you bear more financial responsibility at the time of a claim.

How often should I compare motorcycle insurance policies and quotes?

It’s a good practice to compare quotes and review your existing policy at least once a year, or whenever significant life events occur. These could include buying a new motorcycle, moving to a new address, getting married, or having a significant change in your driving record. The market changes, and so do your needs, so regularly checking ensures you’re always getting the best value and coverage.

Does Florida require specific training or licensing for motorcycles?

Yes, to operate a motorcycle in Florida, you must have a motorcycle endorsement on your driver’s license. Obtaining this typically requires completing a Basic RiderCourse (BRC) from the Motorcycle Safety Foundation or an approved equivalent. This training is not just a legal hurdle; it significantly enhances your riding skills and safety. Often, completing such a course also qualifies you for a discount on your motorcycle insurance premiums.

Navigating the intricacies of motorcycle insurance in Florida might seem complex, but understanding the core principles is straightforward. While the state’s legal mandate isn’t a direct “you must buy this policy today,” the underlying financial responsibility law and the stark realities of accident costs make comprehensive motorcycle insurance an indispensable safeguard for any rider. Your motorcycle is an investment, and your financial future is even more so. Protecting both with the right insurance policy ensures you can continue to enjoy the freedom of the road with genuine peace of mind.

General Information & Professional Disclaimer

Disclaimer

The information provided by bangladeshcountry.com (“we,” “us,” or “our”) on our website is for general informational purposes only. All information on the Site is provided in good faith; however, we make no representation or warranty of any kind, express or implied, regarding the accuracy, adequacy, validity, reliability, availability, or completeness of any information on the Site.

Not Professional Advice The Site cannot and does not contain financial, insurance, legal, medical or professional career advice. The insurance related information is provided for general informational purposes only and is not a substitute for professional advice.

We are not certified financial advisors, insurance agents, or legal professionals. Accordingly, before taking any actions based on such information, we strictly encourage you to consult with the appropriate professionals or certified authorities. We do not provide any kind of professional or financial advice.

THE USE OR RELIANCE OF ANY INFORMATION CONTAINED ON THIS SITE IS SOLELY AT YOUR OWN RISK. We shall not have any liability to you for any loss or damage of any kind incurred as a result of the use of the site or reliance on any information provided on the site.