Choosing health insurance in the United States can feel like navigating a maze, especially with the ever-evolving healthcare landscape. As we move through 2026, understanding the fundamental differences between major plan types remains crucial for making informed decisions that impact both your finances and your access to care. Two acronyms often dominate this conversation: HMO and PPO. These aren’t just different names for health coverage; they represent distinct philosophies in how healthcare is accessed, managed, and paid for. Getting this choice right means aligning your insurance with your lifestyle, your health needs, and your budget, ensuring you get the most value and appropriate care.

Understanding the Core: What Are HMO and PPO Plans?

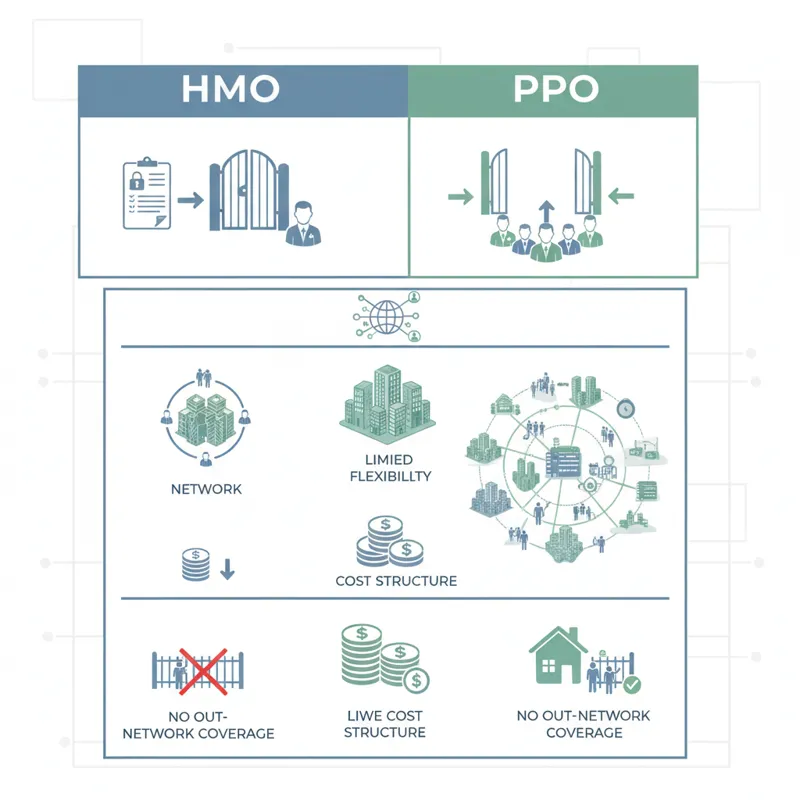

Before diving into the intricate details, it’s essential to grasp the basic operational models of Health Maintenance Organizations (HMOs) and Preferred Provider Organizations (PPOs). Each structure dictates how you interact with doctors, specialists, and hospitals, and significantly influences your out-of-pocket costs.

The HMO: Your Coordinated Care Hub

An HMO plan operates on a managed care model that emphasizes coordinated care and cost control. When you choose an HMO, you select a primary care physician (PCP) within the plan’s network. This PCP becomes your central point of contact for virtually all your healthcare needs. They manage your general health, refer you to specialists when necessary, and approve treatments. The key characteristic of an HMO is its network restriction. Except for emergencies, you typically must receive care from doctors, hospitals, and other providers within the HMO’s defined network. Going outside this network for non-emergency services usually means the plan won’t cover the costs, leaving you responsible for the full bill. This tight control over the network and the referral system helps HMOs keep premiums generally lower than PPO plans.

The PPO: Flexibility and Broader Choice

A PPO plan, by contrast, offers more flexibility and a wider range of choices regarding healthcare providers. With a PPO, you typically don’t need to choose a PCP, and you generally aren’t required to get a referral to see a specialist. You can go directly to any specialist you choose, provided they accept your insurance. PPO plans also have a network of “preferred” providers. When you use doctors or facilities within this network, you pay less out of pocket because they have negotiated lower rates with the insurance company. However, the defining advantage of a PPO is its allowance for out-of-network care. You have the option to see providers outside the network, though your share of the cost (deductibles, copayments, and coinsurance) will be significantly higher. This greater freedom comes with a trade-off, as PPO premiums are generally higher than those for HMO plans.

The Crucial Distinctions: HMO vs PPO Insurance in Detail

The choice between an HMO vs PPO Insurance plan boils down to several critical distinctions, each impacting your healthcare experience and financial outlay. Understanding these nuances is key to selecting the plan that best suits your needs in 2026.

Referrals and Primary Care Physicians (PCPs)

The role of the PCP and the requirement for referrals represent one of the most fundamental differences.

- HMO: A PCP is mandatory. This doctor acts as your “gatekeeper,” coordinating all your care. To see a specialist, you must first get a referral from your PCP. Without a referral, the HMO will likely not cover the specialist visit. This system aims to ensure continuity of care and prevent unnecessary specialist visits, helping manage costs.

- PPO: A PCP is generally not required, and you typically don’t need referrals to see specialists. You can schedule an appointment directly with most in-network specialists. This offers more immediate access to specialized care, which can be a significant advantage for those with ongoing conditions or specific preferences.

Network Flexibility and Provider Choice

The scope of providers you can access without incurring high penalties is another major differentiator.

- HMO: Plans are very restrictive regarding their networks. You must use doctors, hospitals, and labs within the HMO’s network. The network is usually localized, meaning it’s designed for a specific geographic area. If you live, work, and seek care within that area, this might not be an issue.

- PPO: Plans offer much broader flexibility. While they have a “preferred” network of providers where costs are lower, you retain the option to see out-of-network doctors or facilities. This is particularly appealing if you have established relationships with specific doctors who might not be in every plan’s network, or if you travel frequently and need care outside your home area.

Cost Structure: Premiums, Deductibles, Coinsurance, Copayments

The financial architecture of HMO vs PPO Insurance plans varies considerably, influencing your monthly budget and your costs at the point of service.

- Premiums: HMOs generally have lower monthly premiums compared to PPOs. This is due to their managed care model, which often translates to lower overall costs for the insurer. PPOs offer more flexibility, which translates to higher premiums.

- Deductibles: A deductible is the amount you must pay out of pocket before your insurance plan starts paying for covered medical expenses. Many HMOs have lower deductibles, or sometimes even no deductible for certain services like PCP visits. PPOs often come with higher deductibles, especially if you utilize out-of-network care.

- Copayments (Copays): A copay is a fixed amount you pay for a covered service (like a doctor’s visit or prescription drug) after your deductible has been met (though some copays may apply before the deductible, especially for HMOs). HMO copays tend to be lower and more predictable. PPOs will have higher copays for out-of-network care.

- Coinsurance: This is a percentage of the cost of a covered service you pay after you’ve met your deductible. For example, if your coinsurance is 20%, and a service costs $100 after your deductible, you pay $20. PPOs commonly feature coinsurance for both in-network and significantly higher percentages for out-of-network services. HMOs typically use copays rather than coinsurance for most services.

- Out-of-Pocket Maximum: This is the most you’ll have to pay for covered services in a plan year. Once you hit this limit, your insurance plan pays 100% of covered costs. It’s a critical safety net for both plan types. For PPOs, it’s important to understand that in-network and out-of-network spending often contribute to separate out-of-pocket maximums, meaning you could hit both limits in a given year if you use both types of providers.

Out-of-Network Coverage

This is perhaps the most straightforward difference.

- HMO: With very few exceptions (true medical emergencies), HMOs do not cover out-of-network care. If you choose to see a doctor outside your HMO’s network, you are responsible for 100% of the cost.

- PPO: PPOs provide coverage for out-of-network care, but at a higher cost to you. This usually means a higher deductible, higher coinsurance percentage, and potentially less favorable negotiated rates, leading to a much larger bill for the member.

Geographic Considerations

Where you live, work, and travel can heavily influence which plan is more practical.

- HMO: Best suited for individuals or families who live and primarily seek care in a stable, defined geographic area where the HMO has a robust network. They are less ideal if you frequently travel or reside in multiple locations.

- PPO: More advantageous for people who travel often, live in an area with limited HMO networks, or split their time between different locations, potentially even across state lines, as they offer coverage with a wider reach, albeit at a higher cost.

When an HMO Makes Sense: Ideal Scenarios

An HMO plan can be an excellent choice for several specific types of individuals and families. Its structure, while restrictive in some ways, offers distinct advantages. One major draw is cost savings. If you’re highly budget-conscious and lower monthly premiums are a priority, an HMO often delivers. You’ll typically find more predictable costs with fixed copays for most services, and often lower deductibles or even no deductibles for routine care. This predictability can be a significant comfort for managing household expenses. HMOs are ideal for individuals who value coordinated care. If you prefer having a single doctor, your PCP, oversee all your medical needs and guide you through the healthcare system, an HMO’s gatekeeper model will appeal to you. Your PCP becomes familiar with your entire health history, theoretically leading to more integrated and efficient care, avoiding duplicative tests or conflicting treatments. If you have established local providers who are already within a particular HMO network, or if you’re comfortable choosing from the plan’s directory, an HMO can work well. This is especially true if you typically stay within your immediate area for all your medical needs and don’t foresee needing care from doctors outside a localized network. Finally, HMOs are often a good fit for generally healthy individuals who don’t anticipate frequent specialist visits or complex medical needs. If your healthcare primarily consists of annual physicals, occasional urgent care visits, and routine prescriptions, the cost-effectiveness and structured approach of an HMO can be very beneficial.

When a PPO Makes Sense: Ideal Scenarios

For others, the flexibility and broader choice offered by a PPO plan far outweigh its higher costs. A PPO is the clear winner if you seek maximum flexibility and choice in your healthcare providers. If you want the freedom to see any doctor, anywhere, without needing a referral, a PPO provides that autonomy. This is particularly valuable if you prioritize having direct access to specialists without an intermediary step. It’s also an excellent option for individuals who need specific specialists or prefer to continue care with doctors who might not be part of a local HMO network. This could be due to a rare condition, a long-standing relationship with a particular expert, or simply a preference for a doctor renowned in their field, regardless of their network affiliation.Frequent travelers or those who live in different states for parts of the year often find PPOs more practical. Since PPOs offer out-of-network coverage, you have a safety net if you need medical care while away from home. Relying solely on an HMO network when you’re frequently out of its service area can be incredibly limiting and expensive. Individuals with chronic conditions that necessitate regular visits to multiple specialists often benefit from a PPO. The ability to directly schedule appointments with cardiologists, endocrinologists, or neurologists without waiting for a PCP referral can streamline care and reduce administrative hurdles. Ultimately, PPOs are for people willing to pay more for choice and convenience. If higher premiums and potentially higher out-of-pocket costs are acceptable trade-offs for unparalleled freedom in selecting your doctors and avoiding referral requirements, a PPO is likely your preferred plan.

Things People Usually Miss or Misunderstand About HMO vs PPO Insurance

Beyond the basic definitions, several nuances often trip up individuals comparing HMO vs PPO Insurance. Understanding these subtle points can prevent unwelcome surprises down the line. First, “network” isn’t always what it seems. Provider directories, especially online, can be notoriously outdated. A doctor listed as “in-network” today might leave the network tomorrow, or their specific practice location might not be covered. Always call your prospective doctors and the insurance company directly to verify network participation before receiving care. This simple step can save you thousands. Second, many assume emergency care works entirely differently between plans. While both HMOs and PPOs cover true medical emergencies regardless of network status, follow-up care is where the distinction re-emerges. If you’re admitted to an out-of-network hospital for an emergency, an HMO will cover the initial emergency. However, once stable, you might be required to transfer to an in-network facility for continued treatment, or subsequent non-emergency follow-up care (even related to the emergency) might require a referral and be limited to in-network providers. With a PPO, you’ll still have higher out-of-network costs for the emergency, but more flexibility for follow-up. Third, the referral system in HMOs isn’t just an inconvenience; it can be a benefit. While often perceived as a hurdle, your PCP’s role in coordinating care can prevent unnecessary specialist visits, duplicate tests, and ensure all your doctors are on the same page. This integrated approach can lead to more holistic and cost-effective care over time. Fourth, it’s crucial to understand how out-of-pocket maximums work, particularly with PPOs. For PPO plans, there are often separate out-of-pocket maximums for in-network and out-of-network care. This means that if you utilize both types of providers extensively in a year, you could potentially hit both maximums, leading to a much higher overall cost than if you only used in-network providers. Fifth, the “best” plan is not static; it changes with your life. Your health needs in 2026 might be very different from your needs in 2024 or what you project for 2028. A plan perfectly suited for a healthy young adult might be completely inadequate for someone starting a family or managing a new chronic condition. Regularly re-evaluating your plan during open enrollment is key. Finally, always look beyond just the monthly premium. Hidden costs beyond premiums—such as deductibles, copays, and coinsurance—add up quickly. A lower premium HMO might have higher copays for certain services than a higher premium PPO. Conversely, a PPO’s high deductible might mean you pay significant amounts before insurance kicks in. To truly compare, estimate your likely healthcare usage and calculate the total cost of ownership for each plan. Just as you’d thoroughly investigate more than just the monthly payment when shopping for the [Cheapest Renters Insurance](https://www.bangladeshcountry.com/cheapest-renters-insurance/) to understand coverage limits and deductibles, you need to apply the same rigorous analysis to health insurance. Don’t be swayed by just one number.

Key Decision-Making Factors for 2026

Making the right choice between an HMO vs PPO Insurance plan requires a personal inventory of your unique circumstances. Consider these factors:

- Your Health Status and Healthcare Needs: Are you generally healthy and only need preventive care, or do you have chronic conditions requiring frequent specialist visits? If you have complex needs, a PPO might offer smoother access to multiple specialists.

- Your Budget and Risk Tolerance: How much can you comfortably afford in monthly premiums? Are you willing to pay a higher premium for more flexibility (PPO), or would you prefer a lower premium with more predictable, but restricted, costs (HMO)? Consider your tolerance for unexpected out-of-pocket expenses.

- Your Preferred Providers: Do you have specific doctors, specialists, or hospitals you wish to continue seeing? Check if they are in the network for the plans you’re considering. This is a non-negotiable step.

- Your Location and Travel Habits: How important is geographic flexibility? If you travel extensively within the U. S. or live in multiple locations, a PPO’s broader reach could be indispensable. If your life is primarily centered around one locale, an HMO network might suffice.

- Your Comfort with Referrals: Are you comfortable with the “gatekeeper” model of an HMO, where your PCP coordinates all specialist visits? Or do you prefer the autonomy of directly scheduling appointments with specialists as needed?

- Availability in Your Area: Not all plans are available in every geographic region. Your choices may be limited by what insurers offer where you live. This foundational understanding is crucial, much like understanding specific requirements for niche policies such as [Commercial Auto Insurance](https://www.bangladeshcountry.com/commercial-auto-insurance/) which varies by state and business type.

Navigating the Enrollment Process

Once you’ve weighed your options, you’ll need to enroll. The process is generally straightforward but requires attention to deadlines. The primary time to choose or change your health insurance plan is during Open Enrollment. For 2026 coverage, this period typically occurs in late 2025 (e.g., November 1 to January 15, depending on the state and marketplace). If you miss this window, you usually can’t enroll or change plans unless you qualify for a Special Enrollment Period. Special Enrollment Periods are triggered by specific life events, such as getting married, having a baby, losing other health coverage, or moving to a new service area. These periods typically last 60 days from the qualifying event. You can enroll in plans through several avenues:

- Employer-sponsored plans: Many Americans get their health insurance through their job. Your employer will provide information about available HMO vs PPO Insurance options and the enrollment process.

- Health Insurance Marketplace: For individuals and families who don’t have employer-sponsored coverage, the Health Insurance Marketplace (often referred to as Healthcare.gov or state-run marketplaces) is a key resource. Here, you can compare plans and potentially qualify for subsidies to lower your costs. For more information, visit the official U. S. government HealthCare.gov site.

- Directly from insurers: You can also purchase plans directly from insurance companies, though subsidies are generally only available through the Marketplace.

Regardless of where you enroll, take the time to review the “Summary of Benefits and Coverage” (SBC) for each plan. This standardized document makes it easier to compare key features, costs, and coverage details across different plans. Don’t rush; a well-informed decision now can save you stress and money throughout the year.

Frequently Asked Questions (FAQ)

Here are answers to some common questions that arise when comparing HMO vs PPO Insurance plans:

Can I switch from an HMO to a PPO (or vice versa)?

Yes, generally you can switch plans during your employer’s annual open enrollment period or the Health Insurance Marketplace’s open enrollment. You may also be able to switch if you experience a qualifying life event that triggers a Special Enrollment Period.

What if my doctor leaves the network?

This is a common concern. If your doctor leaves an HMO network, you’ll need to choose a new in-network PCP and potentially new specialists, unless the plan offers a transition-of-care provision for ongoing treatment (which is rare for a general doctor leaving). For a PPO, you could continue seeing that doctor, but they would be considered out-of-network, leading to higher costs for you. Always verify your doctor’s network status regularly.

Are prescription drugs covered differently?

Yes, prescription drug coverage can vary significantly between plans and plan types. Both HMOs and PPOs typically have a formulary (a list of covered drugs) and tiered pricing. However, PPOs might offer more flexibility for out-of-network pharmacies or non-formulary drugs (at a much higher cost), while HMOs are usually stricter about sticking to their formulary and network pharmacies. Always check the specific plan’s drug formulary.

Do deductibles apply to copays?

Usually no. Copayments are generally a fixed amount you pay at the time of service, and they typically do not count towards your annual deductible. However, copays do count towards your annual out-of-pocket maximum. It’s important to read your plan’s specific summary of benefits to confirm these details.

What about dental and vision coverage?

Dental and vision coverage are often separate from your primary medical HMO vs PPO Insurance plan. Some comprehensive medical plans may include limited pediatric dental and vision benefits, or offer adult dental/vision as an add-on rider. More often, these are purchased as standalone plans.

Important Disclaimer

Please be aware that the information provided in this article is for general informational purposes only and is not intended as legal, financial, or professional advice. Healthcare regulations and plan offerings are complex and can change frequently. For personalized advice regarding your specific health insurance needs and options, it is always recommended to consult with a licensed insurance professional or qualified financial advisor. This content does not constitute an endorsement of any particular insurance product or provider.

Conclusion

Deciding between an HMO vs PPO Insurance plan is a significant personal financial and health decision that demands careful consideration. There isn’t a universally “best” option; the optimal choice depends entirely on your individual circumstances, preferences, and financial situation in 2026. Whether you prioritize lower monthly costs and coordinated care with an HMO, or you value maximum flexibility and choice in providers with a PPO, understanding these key differences empowers you to make an informed decision.

Just as you’d research specialized policies for your specific assets, such as how you might approach securing [Cat Insurance](https://www.bangladeshcountry.com/cat-insurance/) for a beloved pet, understanding the nuances of your health plan is equally crucial for your wellbeing. Take the time to assess your health needs, crunch the numbers, and verify provider networks. This proactive approach will ensure your health insurance works for you, providing the coverage and access to care you truly need.

General Information & Professional Disclaimer

Disclaimer

The information provided by bangladeshcountry.com (“we,” “us,” or “our”) on our website is for general informational purposes only. All information on the Site is provided in good faith; however, we make no representation or warranty of any kind, express or implied, regarding the accuracy, adequacy, validity, reliability, availability, or completeness of any information on the Site.

Not Professional Advice The Site cannot and does not contain financial, insurance, legal, medical or professional career advice. The insurance related information is provided for general informational purposes only and is not a substitute for professional advice.

We are not certified financial advisors, insurance agents, or legal professionals. Accordingly, before taking any actions based on such information, we strictly encourage you to consult with the appropriate professionals or certified authorities. We do not provide any kind of professional or financial advice.

THE USE OR RELIANCE OF ANY INFORMATION CONTAINED ON THIS SITE IS SOLELY AT YOUR OWN RISK. We shall not have any liability to you for any loss or damage of any kind incurred as a result of the use of the site or reliance on any information provided on the site.