Living in a rental property in 2026 brings its own set of considerations, and among the most vital is securing your belongings and financial stability. Many renters mistakenly believe their landlord’s insurance policy offers them protection, or that their possessions aren’t valuable enough to warrant coverage. Both assumptions can lead to significant financial hardship. The reality is, your landlord’s policy protects the building structure, not your personal property inside it, nor does it cover your liability if someone gets injured in your rented space. Finding the cheapest renters insurance isn’t about cutting corners on protection; it’s about making smart, informed choices to get robust coverage without breaking your budget. This guide aims to demystify the process, helping you identify specific affordable insurance providers and actionable strategies to lower your premiums, ensuring you’re well-protected.

Understanding the Core of Renters Insurance

Before diving into how to find the cheapest renters insurance, it’s crucial to understand what this type of policy actually covers. Renters insurance typically provides three main areas of protection:

- Personal Property Coverage: This protects your belongings from specified perils like fire, smoke, theft, vandalism, and certain weather events (windstorms, hail, lightning). It covers everything from your furniture, electronics, and clothing to kitchenware and decorative items. Policies usually offer either Actual Cash Value (depreciated value) or Replacement Cost Value (cost to buy new), with the latter providing more comprehensive, albeit slightly more expensive, protection.

- Personal Liability Coverage: This is a critical component. If someone is injured in your rental unit or you accidentally cause damage to someone else’s property, this coverage helps pay for legal fees, medical expenses, or repair costs if you’re found responsible. For instance, if a guest slips and falls, or your overflowing bathtub causes damage to the unit below, your liability coverage kicks in.

- Loss of Use Coverage (Additional Living Expenses): If your rental unit becomes uninhabitable due to a covered peril (e.g., a fire), this part of your policy helps cover the additional costs you incur for temporary housing, food, and other necessities while your home is being repaired or you find a new place.

This foundational understanding is key to making educated decisions, ensuring you don’t compromise essential coverage in your pursuit of a lower premium.

Why You Need Renters Insurance in 2026

It’s easy to dismiss renters insurance as an unnecessary expense, especially when you’re already managing rent, utilities, and other monthly bills. However, the financial risks of not having it can be substantial. Consider the following:

- Unexpected Catastrophes: Fires, burst pipes, and severe weather can happen anywhere, anytime. Replacing all your belongings after such an event can cost tens of thousands of dollars out-of-pocket, a burden few can manage instantly.

- Theft and Vandalism: Apartment break-ins, while hopefully rare, are a reality. Your renters insurance can cover the cost of stolen items, from laptops and jewelry to bicycles.

- Personal Responsibility: As a tenant, you are often financially responsible for accidents that occur on your property. A simple accident could lead to a lawsuit that depletes your savings. Many landlords now require renters insurance as a lease condition precisely because of the liability protection it offers, not just to you, but to protect themselves from potential lawsuits indirectly involving their property.

In an increasingly complex world, this safety net is not just a nice-to-have; it’s a fundamental component of financial planning, providing peace of mind far exceeding its modest cost.

Average Renters Insurance Costs in 2026

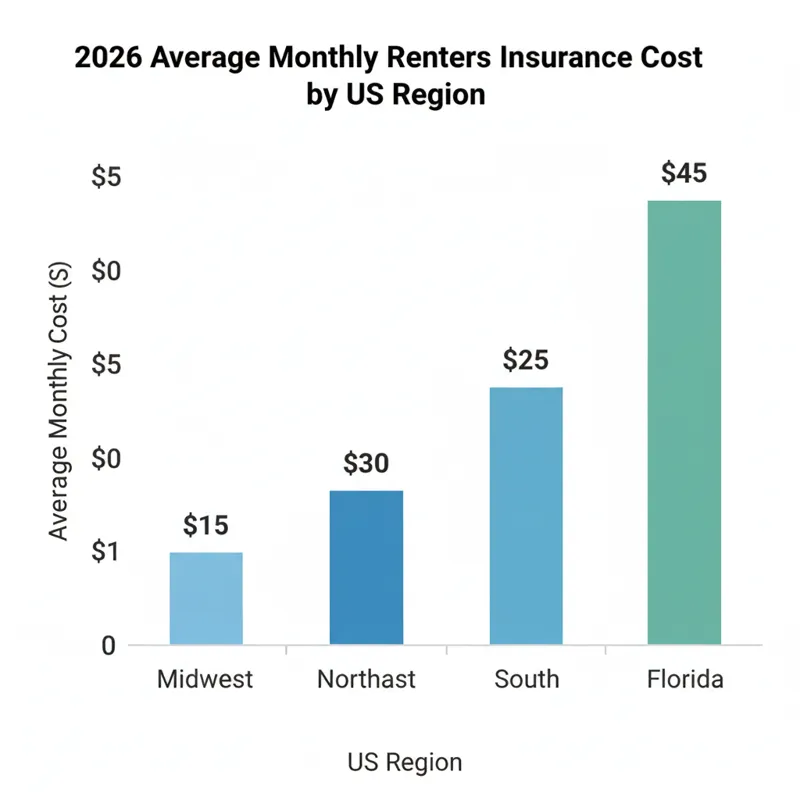

The good news is that renters insurance is typically very affordable. In 2026, the national average for renters insurance generally falls between $12 to $25 per month, or roughly $150 to $300 per year. However, this average can fluctuate significantly based on several key factors:

- Location: Premiums vary by state, city, and even zip code. Areas with higher crime rates or a greater risk of natural disasters (like hurricanes or tornadoes) will typically have higher rates.

- Coverage Limits: The amount of personal property and liability coverage you choose directly impacts your premium. Higher limits mean higher costs.

- Deductible: This is the amount you pay out-of-pocket before your insurance kicks in. A higher deductible usually leads to a lower monthly premium, but means you’ll pay more upfront if you file a claim.

- Claims History: A history of previous insurance claims can increase your rates.

- Credit Score: In many states, your credit score can influence your insurance premium. A higher score often indicates lower risk, leading to better rates.

- Insurer: Different companies have different pricing models, making shopping around essential for finding the cheapest renters insurance.

Understanding these variables helps you tailor a policy that meets your needs without overpaying.

Best Cheap Renters Insurance Companies for 2026

When searching for the cheapest renters insurance, certain providers consistently rank well for affordability and value. Remember that rates are personalized, so getting quotes from multiple providers is crucial. Here are some of the top contenders in 2026:

Lemonade

Known for its tech-forward approach and quick, AI-powered claims process, Lemonade often offers some of the lowest premiums, especially for younger renters and those seeking basic coverage. Their policies are straightforward, and they have a strong focus on social impact by donating leftover premiums to charities.

State Farm

One of the largest insurers in the U. S., State Farm provides competitive rates and a wide network of local agents. While not always the absolute cheapest upfront, their bundling discounts (especially with auto insurance) can make them highly economical. They are also known for strong customer service.

Allstate

Allstate is another major player offering comprehensive renters insurance. They provide various discounts, including multi-policy and security system discounts, which can significantly reduce your premium. Their online tools and agent support make the quote process accessible.

GEICO

Famous for its auto insurance, GEICO also offers affordable renters insurance policies, often through partnerships with other carriers. Their online platform makes getting a quick quote simple, and their multi-policy discounts are a strong incentive for existing customers.

Progressive

Similar to GEICO, Progressive is well-known for competitive pricing, particularly when bundling. They offer a range of customizable options, making it easier to find a policy that fits your budget and specific coverage needs.

Liberty Mutual

Liberty Mutual provides a variety of discounts that can help lower your renters insurance costs, such as multi-policy, claims-free, and even early shopper discounts. They offer a good balance of affordable rates and customizable coverage.

Hippo

Hippo is a newer, technology-driven insurer focusing on proactive home protection. Their renters policies are often bundled with smart home devices, and they aim to offer modern, comprehensive coverage at competitive prices, particularly for those in urban areas.

Nationwide

Nationwide offers a solid range of renters insurance options with various discounts, including multi-policy, protective device discounts, and even a “prior insurance” discount. They provide a reliable option for those looking for comprehensive coverage from a reputable company.

Comparing quotes from these providers is your best bet for finding the cheapest renters insurance tailored to your unique situation.

Actionable Strategies to Get the Cheapest Renters Insurance

Finding truly affordable renters insurance isn’t just about picking the right company; it’s also about implementing smart strategies.

1. Compare Quotes from Multiple Providers

This is arguably the most impactful strategy. Insurance companies use different underwriting models, leading to significant price variations for the exact same coverage. Use online comparison tools or contact several companies directly to get personalized quotes. Don’t settle for the first quote you receive.

2. Bundle Your Policies

If you have car insurance, consider bundling your renters policy with the same provider. Most insurers offer substantial multi-policy discounts, often saving you 10% to 20% or more on both premiums. This is one of the most effective ways to lower your overall insurance costs.

3. Choose a Higher Deductible

Opting for a higher deductible (e.g., $500 or $1,000 instead of $250) will lower your monthly premium. Just ensure you have enough in savings to cover that deductible if you need to file a claim. This strategy is best for those who prefer to pay less regularly and are comfortable with a larger out-of-pocket expense in the event of an incident.

4. Accurately Assess Your Coverage Needs

Don’t over-insure, but don’t under-insure either. Create a detailed home inventory to accurately estimate the value of your personal property. Use an online calculator or spreadsheet. If you have minimal belongings, you might need less personal property coverage, which can lower your premium. Conversely, if you have high-value items, you might need special endorsements or riders, which can increase cost but are crucial for full protection.

5. Look for Available Discounts

Many insurers offer a range of discounts beyond bundling:

- Security Devices: Smoke detectors, fire alarms, home security systems, and deadbolt locks can earn you discounts.

- Claims-Free: If you haven’t filed a claim for a certain period, you might qualify for a discount.

- Automatic Payments: Setting up auto-pay from your bank account can sometimes lead to a small discount.

- Non-Smoker: Some insurers offer discounts for non-smokers.

- Good Student: If you’re a student, some providers offer discounts for maintaining a good GPA.

- Paperless Billing: Opting for electronic statements can sometimes reduce your premium.

Always ask your agent about every discount you might be eligible for.

6. Maintain a Good Credit Score

In states where it’s allowed, insurers often use credit-based insurance scores to help determine premiums. A higher credit score generally indicates a lower risk profile, potentially leading to better rates. Paying your bills on time and managing your debt responsibly can indirectly help you get the cheapest renters insurance.

What Most People Get Wrong About Renters Insurance

Even savvy individuals often overlook critical aspects of their renters insurance, leading to potential gaps in coverage or unnecessary expenses.

Underestimating Personal Property Value

Many renters vastly underestimate how much it would cost to replace all their belongings. They might think “I don’t own much,” but if you add up the cost of your clothes, shoes, electronics, furniture, kitchenware, books, and decor, it can easily reach $20,000 to $50,000 or more. Failing to create a home inventory and accurately valuing your items can leave you significantly underinsured after a loss. Even specific apparel for special events, such as ultimate tea-length dresses for weddings, should be accounted for if they hold significant value.

Assuming the Landlord’s Policy Covers Them

This is perhaps the most common misconception. Your landlord’s insurance covers the physical building itself and their liability, not your personal property or your liability as a tenant. If a fire destroys the building, your landlord’s policy pays to rebuild, but it won’t replace your burned furniture or clothing. This is why renters insurance is so vital.

Ignoring Sub-Limits for Valuables

Standard renters insurance policies often have “sub-limits” for specific categories of high-value items like jewelry, furs, firearms, artwork, or collectibles. For example, a policy might have a $1,500 sub-limit for jewelry, meaning even if your overall personal property coverage is $30,000, they’ll only pay up to $1,500 for stolen jewelry. If you own expensive items in these categories, you’ll need to purchase additional coverage (often called a “rider” or “endorsement”) to ensure they’re fully protected. This is crucial even for hobbyists who might own specialized equipment, perhaps even professional-grade items like top-tier convection oven models for a home baking business, or for culinary enthusiasts investing in the best commercial rice cooker picks for 2026, as these often exceed typical item limits.

Not Understanding Actual Cash Value vs. Replacement Cost

Many policies default to Actual Cash Value (ACV) for personal property. This means if your 5-year-old laptop is stolen, the insurer pays out its current depreciated value, not the cost to buy a brand new one. Replacement Cost Value (RCV) coverage, while slightly more expensive, pays out the cost to replace the item with a new one of similar kind and quality. Always confirm which type of coverage your policy offers and consider upgrading to RCV for better protection.

Neglecting to Update Their Policy

Life changes: you buy new furniture, upgrade electronics, get married, or acquire valuable collectibles. Your renters insurance policy should evolve with your life. Review your coverage annually to ensure it still accurately reflects the value of your possessions and your current living situation. Not updating your policy could lead to being underinsured when you need it most.

The Application Process: What to Expect

Applying for renters insurance in 2026 is generally a quick and straightforward process, often completed online in minutes. Here’s what you’ll typically need:

- Personal Information: Your name, date of birth, and contact details.

- Rental Address: The full address of the property you’re renting.

- Desired Coverage Amounts: An estimate of the value of your personal property and how much liability coverage you want (e.g., $15,000 in personal property, $100,000 in liability).

- Deductible Preference: Your chosen deductible amount (e.g., $500, $1,000).

- Basic Security Information: Details about smoke detectors, fire extinguishers, or any alarm systems in your unit.

- Payment Method: Banking information for automatic payments.

Most online platforms will walk you through these steps, providing instant quotes and allowing you to customize your policy before purchase. For more complex situations or questions, speaking with an agent can be beneficial. Checking out reliable sources like Wikipedia’s entry on renters’ insurance can also provide a good foundational understanding before you start the application process.

Frequently Asked Questions About Cheapest Renters Insurance

Q: How can I find the absolute cheapest renters insurance?

A: The absolute cheapest policy will vary for everyone based on location, coverage needs, and personal factors. Your best approach is to get multiple quotes from different providers (e.g., Lemonade, State Farm, GEICO), bundle with existing policies if possible, choose a higher deductible you can afford, and inquire about every discount available.

Q: Is a low-cost renters insurance policy sufficient?

A: A low-cost policy can be sufficient if it provides adequate personal property coverage to replace your belongings and enough liability coverage to protect your assets. The goal isn’t just the lowest premium, but the best value: robust coverage at an affordable price. Always ensure your policy covers the actual value of your possessions and appropriate liability limits.

Q: Does renters insurance cover roommates?

A: Typically, a standard renters insurance policy only covers the policyholder and their immediate family members living in the same household. If you have roommates who are not family, they would generally need their own separate renters insurance policy to cover their belongings and liability. Some insurers might offer endorsements to include roommates, but this is less common.

Q: Will my renters insurance premium increase if I file a claim?

A: Yes, similar to auto insurance, filing a claim (especially multiple claims) can lead to an increase in your premium upon renewal. Insurers view a claims history as an indicator of higher future risk. This is why it’s important to weigh the cost of small damages against your deductible and potential premium increase before filing a claim.

Q: Is renters insurance tax-deductible?

A: For most individuals, renters insurance premiums are not tax-deductible. The exception might be if you use a portion of your rental unit exclusively and regularly for a home-based business, in which case a portion might be deductible as a business expense. Consult a tax professional for specific advice.

Q: What’s the difference between replacement cost and actual cash value?

A: Replacement Cost Value (RCV) pays to replace your damaged or stolen items with new ones of similar kind and quality, without deduction for depreciation. Actual Cash Value (ACV) pays the depreciated value of your items, meaning it factors in wear and tear. RCV policies offer more comprehensive protection but typically come with slightly higher premiums. When seeking the cheapest renters insurance, ACV policies are often presented first, so ensure you understand the difference.

Q: How can I estimate the value of my personal property?

A: The best way is to create a home inventory. Go room by room, listing all your possessions. Include details like make, model, and estimated value. Take photos or videos. Keep receipts for significant purchases. Many apps and online spreadsheets are available to help with this process. This inventory will be invaluable if you ever need to file a claim and helps you determine adequate coverage limits.

Final Thoughts on Securing Affordable Renters Insurance

In 2026, finding the cheapest renters insurance is more accessible and crucial than ever. It’s not about skimping on protection but about making informed decisions to secure comprehensive coverage at a price that fits your budget. By understanding what renters insurance covers, comparing quotes diligently, taking advantage of discounts, and accurately assessing your needs, you can protect your financial future against unforeseen events. Don’t wait for a disaster to realize the value of this essential safeguard. Take the proactive step today to secure your home and wallet, ensuring peace of mind for you and your loved ones. For further financial guidance, resources like the U. S. government’s money and credit information can offer broader insights into managing your finances effectively.

General Information & Professional Disclaimer

Disclaimer

The information provided by bangladeshcountry.com (“we,” “us,” or “our”) on our website is for general informational purposes only. All information on the Site is provided in good faith; however, we make no representation or warranty of any kind, express or implied, regarding the accuracy, adequacy, validity, reliability, availability, or completeness of any information on the Site.

Not Professional Advice The Site cannot and does not contain financial, insurance, legal, or professional career advice. The insurance and information is provided for general informational purposes only and is not a substitute for professional advice.

We are not certified financial advisors, insurance agents, or legal professionals. Accordingly, before taking any actions based on such information, we strictly encourage you to consult with the appropriate professionals or certified authorities. We do not provide any kind of professional or financial advice.

THE USE OR RELIANCE OF ANY INFORMATION CONTAINED ON THIS SITE IS SOLELY AT YOUR OWN RISK. We shall not have any liability to you for any loss or damage of any kind incurred as a result of the use of the site or reliance on any information provided on the site.