Navigating car insurance in Florida can feel like a complex journey, even for seasoned residents. The Sunshine State, with its unique blend of bustling tourist destinations, dense population centers, and distinct legal framework, presents a particular set of challenges and considerations when it comes to protecting your vehicle. As we move through 2026, understanding the specifics of Florida’s auto insurance market isn’t just about compliance; it’s about smart financial planning and ensuring genuine peace of mind on the road.

Understanding Florida’s Unique Auto Insurance Landscape

Florida stands out with its “no-fault” insurance system, a concept often misunderstood by those new to the state or unfamiliar with its implications. This system fundamentally alters how claims are handled after an accident, focusing on immediate medical care rather than assigning blame right away. It’s a critical aspect of no-fault insurance designed to streamline medical payments, but it doesn’t mean fault is irrelevant for property damage or serious injuries. This no-fault environment, coupled with factors like frequent severe weather events, a high number of uninsured drivers, and a litigious culture, contributes to Florida’s reputation for relatively high car insurance premiums. The state’s diverse driving conditions, from congested urban highways to rural roads, also play a significant role. Therefore, selecting the right car insurance Florida policy requires a strategic approach beyond just meeting minimum requirements.

The Core of Florida’s No-Fault System: Personal Injury Protection (PIP)

At the heart of Florida’s no-fault law is Personal Injury Protection (PIP). This coverage is designed to pay for your medical expenses, lost wages, and other related costs, regardless of who caused the accident. This is a crucial distinction. Instead of waiting for fault to be determined, your own insurance company pays for your initial medical treatment up to your PIP limit. While PIP aims to expedite care, its limitations are often overlooked. The standard PIP policy only covers a fraction of potential medical costs, which can quickly be exhausted in serious accidents. Understanding these boundaries is key to assessing whether you need additional protection.

Minimum Auto Insurance Requirements in Florida (2026)

For any vehicle registered in Florida, specific minimum coverage types are legally mandated. These requirements are set by the state to ensure that drivers have a basic level of financial responsibility. It’s important to remember that these are minimums, and relying solely on them can leave you significantly exposed in the event of a serious accident. Here’s what you absolutely need for car insurance Florida:

- Personal Injury Protection (PIP): You must carry at least $10,000 in PIP coverage. This covers 80% of necessary and reasonable medical expenses, 60% of lost wages, and 100% of replacement services (like hiring someone to do household tasks you can’t perform) up to your policy limit, regardless of fault. A significant point to note for 2026 is that the Florida Legislature has regularly debated adjustments to these PIP requirements, so it’s always wise to check the latest specifics from official sources like the Florida Office of Insurance Regulation.

- Property Damage Liability (PDL): A minimum of $10,000 in PDL coverage is required. This coverage pays for damage you cause to another person’s property in an accident, such as their vehicle, fence, or building.

It’s critical to understand what these minimums don’t cover. They do not protect you from:

- Damage to your own vehicle.

- Medical expenses for others if you’re at fault (beyond your PIP if it applies to them).

- Bodily injury to others if you cause an accident.

Many drivers, particularly those looking for the cheapest car insurance FL, often stop at these minimums. However, this approach carries substantial financial risk, as a serious accident could quickly exceed these limits, leaving you personally liable for significant costs.

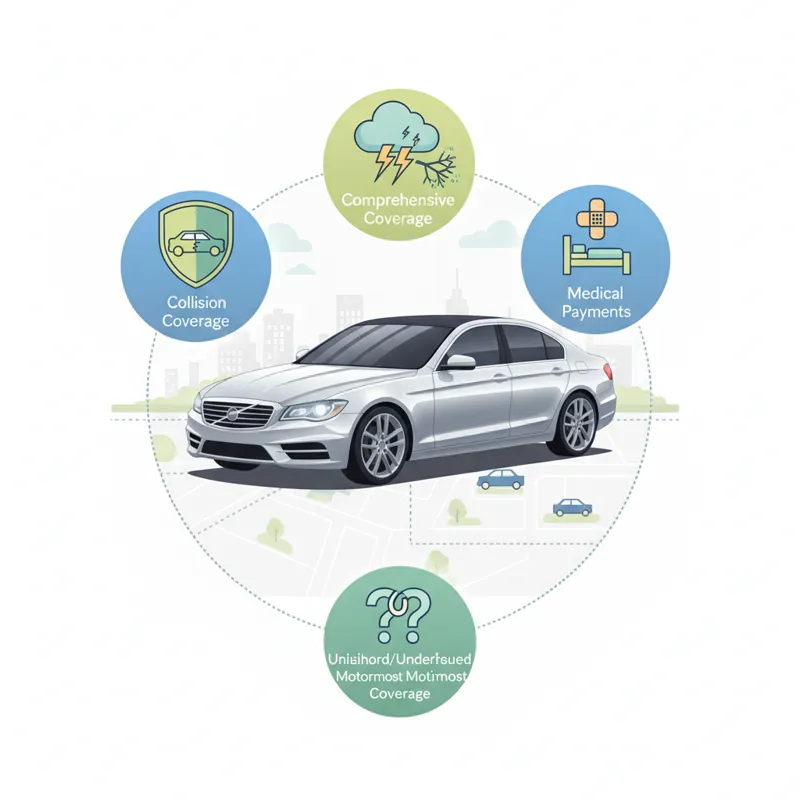

Beyond the Basics: Recommended Additional Coverage Options

While Florida’s minimum requirements provide a baseline, they are rarely sufficient for comprehensive protection. A knowledgeable professional would always advise considering additional coverages to truly safeguard your assets and financial future. These options enhance your car insurance Florida policy significantly.

Bodily Injury Liability (BIL)

This is perhaps the most crucial optional coverage in Florida. BIL pays for medical expenses, lost wages, and pain and suffering for others if you are at fault in an accident. Although Florida is a no-fault state for your medical injuries, if you cause an accident and another party’s injuries exceed their PIP limits (or are severe enough to meet a legal threshold), you can be sued. Without BIL, you’d be personally responsible for those damages. Typical recommendations often start at $25,000 per person and $50,000 per accident (25/50).

Uninsured/Underinsured Motorist (UM/UIM)

Florida has one of the highest rates of uninsured drivers in the country. This makes UM/UIM coverage exceptionally important. If an uninsured or underinsured driver hits you, this coverage pays for your medical expenses and, in some cases, lost wages and pain and suffering, up to your policy limits. It’s an essential layer of protection against the financial irresponsibility of others. Many prioritize finding the right chai tea bags for their morning ritual, but overlooking UM/UIM can leave you exposed to much greater financial headaches than a weak cup of tea.

Collision Coverage

This pays for damage to your own vehicle if you hit another car, an object (like a tree or pole), or if your car rolls over. If you have a car loan or lease, collision coverage is almost always required by your lender. It’s a fundamental component of protecting your asset.

Comprehensive Coverage

Comprehensive coverage protects your vehicle from non-collision incidents. This includes damage from theft, vandalism, fire, natural disasters (like hurricanes or floods, which are highly relevant in Florida), falling objects, or hitting an animal. Given Florida’s susceptibility to severe weather, comprehensive coverage is often considered indispensable.

Medical Payments (MedPay)

While PIP covers 80% of your medical bills, MedPay can cover the remaining 20% and other medical expenses for you and your passengers, regardless of fault, often with a lower deductible or no deductible at all. It can act as a valuable supplement to your PIP, especially if you have a high-deductible health insurance plan.

Other Useful Add-ons

- Rental Car Reimbursement: Covers the cost of a rental car while your vehicle is being repaired after a covered claim.

- Roadside Assistance: Provides services like towing, jump-starts, tire changes, and fuel delivery.

- Gap Insurance: If your car is totaled and you owe more on your loan than the car’s actual cash value, gap insurance pays the difference.

What Drives Car Insurance Costs in Florida?

It’s no secret that average car insurance cost in Florida tends to be higher than the national average. Several interwoven factors contribute to this reality, and understanding them helps you strategize on how to manage your premiums.

Florida-Specific Environmental and Demographic Factors:

- Severe Weather: Hurricanes, tropical storms, and heavy rainfall are common. These events lead to a high volume of comprehensive claims (flooding, wind damage, falling trees) and increase the overall risk profile for insurers.

- High Population Density and Tourism: More drivers on the road, including many unfamiliar with local conditions, naturally lead to more accidents. Tourist areas often see higher claim rates.

- High Number of Uninsured Motorists: As mentioned, Florida’s high rate of drivers without insurance means insurers face more UM claims, which they factor into overall pricing.

- Fraud and Litigation: Florida has a history of high insurance fraud rates (particularly PIP fraud) and a litigious environment. Lawsuits drive up costs for insurers, which are then passed on to consumers.

- Construction Costs and Parts Availability: The cost of vehicle repairs, including labor and parts, has risen steadily. Supply chain issues and inflation also play a role in increasing claim payouts.

Driver and Vehicle-Specific Factors:

- Driving Record: Accidents, speeding tickets, and other moving violations significantly increase your premiums. Florida insurers heavily weigh your history.

- Age and Experience: Younger, less experienced drivers typically pay more due to higher statistical risk.

- Vehicle Type: Expensive, high-performance, or commonly stolen vehicles cost more to insure. Safety features, repair costs, and theft rates specific to a model all factor in.

- Credit History: In Florida, like many states, your credit-based insurance score can heavily influence your premiums. A strong credit history often correlates with lower rates.

- Location (ZIP Code): Urban areas with higher traffic density, crime rates, or historical accident data will generally have higher premiums than rural areas.

- Coverage and Deductibles: The more coverage you opt for, and the lower your deductibles, the higher your premiums will be.

How to Find the Cheapest Car Insurance FL Without Sacrificing Protection

Finding affordable car insurance in Florida requires diligence and a strategic approach. It’s not just about searching for “cheapest car insurance FL” but about finding the best value that offers adequate protection for your specific situation.

1. Compare Florida Auto Insurance Quotes Extensively

This is the single most effective strategy. Rates vary dramatically between insurance companies, even for the exact same coverage. Don’t settle for the first quote you receive. Use online comparison tools, independent agents, or directly contact multiple insurers. Aim to compare auto insurance rates Florida from at least 3-5 different providers every year or whenever your circumstances change (new car, new address, marriage).

2. Bundle Your Policies

Most insurance companies offer discounts if you bundle multiple policies, such as combining your car insurance with homeowners, renters, or even boat insurance. This can lead to substantial savings across all your policies.

3. Maximize Available Discounts

Insurers offer a wide array of discounts. Always ask what’s available:

- Good Driver/Accident-Free: Rewarded for a clean driving record.

- Multi-Car: Insuring multiple vehicles with the same company.

- Safe Driver Programs (Telematics): Many companies offer programs where a device monitors your driving habits (speed, braking, mileage). Good habits can lead to significant savings.

- Anti-Theft Devices: Alarms, tracking systems, or VIN etching can reduce comprehensive premiums.

- Defensive Driving Courses: Completing an approved defensive driving course can often earn you a discount, especially for younger drivers.

- Good Student: Students with good grades can qualify for discounts.

- Pay-in-Full: Paying your premium in one lump sum rather than monthly installments.

- Loyalty Discounts: For long-term customers.

4. Choose Higher Deductibles

Your deductible is the amount you pay out of pocket before your insurance coverage kicks in for collision and comprehensive claims. Choosing a higher deductible (e.g., $1,000 instead of $500) will lower your premium. Just ensure you have enough in savings to cover that deductible if you need to file a claim.

5. Consider Your Vehicle Choice

Before buying a new car, research its insurance costs. Some vehicles are inherently more expensive to insure due to their value, repair costs, theft rates, or safety ratings. A more modest, safer vehicle can significantly reduce your car insurance Florida expenses.

6. Maintain a Good Credit Score

As mentioned, your credit-based insurance score is a major factor in Florida. Keeping your credit healthy by paying bills on time and managing debt responsibly can lead to lower insurance rates.

7. Review Your Coverage Annually

Your insurance needs change over time. Has your car depreciated significantly? Do you drive less? Have you paid off your loan? You might be able to reduce collision and comprehensive coverage on older vehicles. Periodically assess if your current level of protection still aligns with your assets and risk tolerance. While it might not directly relate to your car insurance, taking moments to research things like the ultimate tea tree shaping cream secrets for personal care is a good habit, but never forget to regularly review critical financial details like your policy.

Things People Usually Miss About Car Insurance Florida

Despite Florida’s unique insurance landscape, certain nuances often escape even savvy drivers. Being aware of these points can prevent costly surprises.

The “No-Fault” System Isn’t an Absolution of Responsibility

While PIP pays for your immediate medical bills regardless of fault, this doesn’t mean blame is never assigned. For property damage and severe injuries (those exceeding PIP thresholds or meeting specific legal criteria), fault absolutely matters. You can still be sued for significant damages if you’re deemed responsible for an accident. This is where Bodily Injury Liability (BIL) becomes paramount, despite not being a mandatory minimum.

PIP Limits Are Easily Exhausted

The $10,000 PIP limit might sound substantial, but medical costs, especially for emergency care, surgeries, or prolonged therapy, can quickly surpass this. Even a relatively minor car accident can rack up thousands in medical bills within days. Without supplemental coverage like Medical Payments or robust health insurance, you could face significant out-of-pocket expenses.

The Critical Role of Uninsured/Underinsured Motorist (UM/UIM) Coverage

Many drivers decline UM/UIM coverage to save a few dollars, but given Florida’s high percentage of uninsured drivers, this is a risky gamble. If you’re hit by someone without adequate insurance, your UM/UIM policy could be your only recourse for covering your medical bills, lost wages, and pain and suffering. It’s often one of the most cost-effective forms of protection against a very real and common threat on Florida roads.

Your Credit Score’s Impact is Significant

Many drivers don’t realize that their credit score plays a substantial role in determining their car insurance premiums in Florida. Insurers use credit-based insurance scores as a predictor of future claim likelihood. A lower credit score can translate to considerably higher rates, even if you have a perfect driving record. Proactively managing your credit can indirectly save you money on insurance.

Coverage Limits vs. Policy Limits

It’s important to differentiate between the maximum amount an insurer will pay per person versus per accident for liability coverages like BIL. For example, a 25/50/25 policy means $25,000 for bodily injury per person, $50,000 for bodily injury per accident, and $25,000 for property damage per accident. Understanding these numbers is crucial when assessing your true exposure.

Navigating the Claims Process in Florida

Even with the best coverage, the true test of your car insurance Florida policy comes during a claim. Knowing what to do can simplify an otherwise stressful situation.

1. At the Scene of an Accident

Your first priority is safety. Move to a safe location if possible, check for injuries, and call 911 if there are injuries, significant damage, or if the accident impedes traffic. Exchange information with the other driver(s): name, contact, insurance company and policy number, driver’s license number, and license plate number. Do not admit fault. Document everything with photos and videos of the vehicles, accident scene, and any visible injuries.

2. Report to Your Insurer Promptly

Contact your insurance company as soon as reasonably possible, even if you’re unsure about filing a claim. Delays can complicate the process. Provide them with all the details and documentation you collected.

3. Cooperate with the Adjuster

Your insurer will assign an adjuster to investigate the claim. They will review the police report, photos, statements, and assess vehicle damage. Be honest and cooperative, but also be clear about what your policy covers and your rights.

4. Understand Your Repair Options and Settlement

For vehicle damage, your insurer might recommend repair shops or allow you to choose your own. Understand the estimate and what your deductible will be. For injury claims, PIP will kick in first. Be aware of the settlement process, especially if serious injuries lead to a bodily injury liability claim against an at-fault driver. Your insurer will work on your behalf, but staying informed is key.

Future Trends in Florida Auto Insurance (2026 Perspective)

The car insurance landscape is constantly evolving, and Florida is no exception. Looking ahead from 2026, several trends are likely to shape how we protect our vehicles.

Impact of Advanced Driver-Assistance Systems (ADAS) and Autonomous Vehicles

As more vehicles come equipped with ADAS features like automatic emergency braking, lane-keeping assist, and adaptive cruise control, we expect to see these systems positively influence accident rates, potentially leading to lower premiums. Fully autonomous vehicles are still in early stages, but their eventual widespread adoption could fundamentally alter liability models, shifting focus from driver fault to software or manufacturer liability. Florida, always at the forefront of transportation innovation, will likely be an early adopter of new regulatory frameworks for these technologies.

Climate Change and Natural Disaster Risk Assessment

With increasing frequency and intensity of hurricanes and other severe weather events, insurers in Florida will continue to refine their risk models. This could lead to more localized premium adjustments, with properties in high-risk flood or hurricane zones seeing greater cost increases. The availability and pricing of comprehensive coverage, which protects against these perils, will remain a critical concern for car insurance Florida consumers.

Data Analytics and Telematics Refinement

The use of telematics and data analytics will become even more sophisticated. Expect more personalized pricing based on individual driving behavior, rather than broad demographic classifications. Privacy concerns will continue to be a debate, but the allure of lower premiums will likely drive further adoption of these usage-based insurance programs.

Regulatory Landscape

Florida’s insurance market is dynamic. Discussions around potential changes to the no-fault system, caps on litigation, and strategies to combat insurance fraud are ongoing. Any significant legislative changes could have widespread impacts on policy structures and premium costs for all drivers.

Frequently Asked Questions About Car Insurance Florida

Understanding car insurance Florida can spark many questions. Here are some commonly asked ones:

Is Florida really a no-fault state?

Yes, Florida operates under a no-fault system for personal injuries. This means your own Personal Injury Protection (PIP) insurance pays for your medical expenses and lost wages, up to your policy limit, regardless of who caused the accident. However, fault can still be determined for property damage and for significant injuries that exceed PIP limits or meet certain legal thresholds.

What is PIP and why do I need it?

PIP, or Personal Injury Protection, is a mandatory coverage in Florida. It pays for 80% of your medical bills, 60% of lost wages, and other related expenses up to $10,000 (or higher if you choose additional coverage) if you’re injured in a car accident, regardless of who was at fault. You need it because it’s a legal requirement and provides immediate access to funds for medical care.

How much does car insurance cost in Florida on average?

The average car insurance cost in Florida is typically higher than the national average, often due to factors like severe weather, dense population, high rates of uninsured drivers, and a litigious environment. Exact costs vary significantly based on your driving record, age, vehicle type, location, credit score, and chosen coverage limits. It’s essential to compare Florida auto insurance quotes to get a precise estimate for your situation.

Can I drive without any car insurance in Florida?

No. It is illegal to drive in Florida without at least the minimum required insurance: $10,000 in Personal Injury Protection (PIP) and $10,000 in Property Damage Liability (PDL). Driving without insurance can lead to severe penalties, including fines, license suspension, and vehicle registration suspension.

What happens if I get into an accident without insurance?

If you’re involved in an accident in Florida without the legally required insurance, you face serious consequences. Your driver’s license and vehicle registration will likely be suspended for up to three years. You’ll also be personally responsible for all damages and injuries you cause, and you could face significant fines and court costs. Reinstatement often requires proof of financial responsibility (e.g., filing an SR-22).

How often should I compare car insurance quotes?

It’s a good practice to compare car insurance quotes from multiple providers at least once a year, typically before your policy renews. You should also compare quotes whenever you experience a significant life event, such as buying a new car, moving to a new ZIP code, adding a new driver to your policy, or getting married. Even if you’re happy with your current insurer, comparing can reveal better rates or coverage options you might be missing. For many, finding the best caffeine-free tea choices for 2026 is a yearly ritual, and comparing insurance should be too.

Protecting your vehicle and your financial future in Florida demands a clear understanding of the state’s unique insurance landscape. By moving beyond the minimum requirements and strategically selecting coverage that fits your needs, you can navigate the complexities with confidence. Always compare Florida auto insurance quotes diligently, leverage available discounts, and review your policy regularly to ensure you have the best coverage at the most competitive price. Don’t let the pursuit of the cheapest car insurance FL compromise the security you truly need.

General Information & Professional Disclaimer

Disclaimer

The information provided by bangladeshcountry.com (“we,” “us,” or “our”) on our website is for general informational purposes only. All information on the Site is provided in good faith; however, we make no representation or warranty of any kind, express or implied, regarding the accuracy, adequacy, validity, reliability, availability, or completeness of any information on the Site.

Not Professional Advice The Site cannot and does not contain financial, insurance, legal, medical or professional career advice. The insurance related information is provided for general informational purposes only and is not a substitute for professional advice.

We are not certified financial advisors, insurance agents, or legal professionals. Accordingly, before taking any actions based on such information, we strictly encourage you to consult with the appropriate professionals or certified authorities. We do not provide any kind of professional or financial advice.

THE USE OR RELIANCE OF ANY INFORMATION CONTAINED ON THIS SITE IS SOLELY AT YOUR OWN RISK. We shall not have any liability to you for any loss or damage of any kind incurred as a result of the use of the site or reliance on any information provided on the site.