As a contractor in the United States, your daily work involves a dynamic environment, managing projects, teams, and client expectations. From residential renovations to large-scale commercial builds, every job carries inherent risks. While you focus on delivering quality craftsmanship and meeting deadlines, an unexpected accident or unforeseen incident can quickly derail your business, leading to significant financial losses and even legal battles. This is where robust protection, specifically General Liability Insurance for Contractors, becomes not just a recommendation but an absolute necessity in 2026.

Understanding General Liability Insurance for Contractors: Your Essential Shield

General Liability Insurance, often referred to as CGL (Commercial General Liability), acts as a fundamental safeguard for your contracting business. It protects you from claims of bodily injury or property damage that might arise during your operations, along with other potential liabilities. Think of it as your business’s financial buffer against the unpredictable. Without it, a seemingly minor incident could escalate into a devastating lawsuit, threatening your company’s solvency and reputation. For any builder, remodeler, electrician, plumber, or general contractor, understanding and securing adequate general liability coverage isn’t just good practice; it’s a cornerstone of sustainable business operation in today’s complex legal landscape.

What Does General Liability Insurance for Contractors Actually Cover?

The core of a general liability policy is its promise to cover specific types of claims. Let’s break down the key areas it addresses:

Bodily Injury

This coverage steps in if someone other than an employee is injured on your job site or due to your operations, and you’re found legally responsible. For example, if a client’s child trips over your tools left out during a kitchen remodel and breaks an arm, your policy would help cover their medical expenses and potential legal fees if they sue. It also applies if a visitor falls on a slippery floor you just finished cleaning in a commercial space.

Property Damage

This is crucial for contractors. If your work or operations accidentally damage property belonging to someone else, this coverage pays for the repairs or replacement. Imagine your crew accidentally punctures a water pipe while drilling into a wall, causing extensive water damage to a client’s home. Your general liability insurance would cover the cost to repair the damaged pipe and restore the affected areas. Or, if a piece of heavy equipment accidentally scrapes a client’s newly paved driveway, the policy would help pay for its repair.

Personal and Advertising Injury

While less common in day-to-day operations, this aspect of commercial general liability for builders is important. It covers claims like libel, slander, copyright infringement, or false advertising. For instance, if you inadvertently use a competitor’s copyrighted slogan in your marketing materials, or if a disgruntled former client alleges defamation against your company, this coverage can help with legal defense costs and any settlement or judgment.

Medical Payments

This offers a more immediate, no-fault coverage for minor injuries sustained by non-employees on your premises or due to your operations. It’s typically a lower limit coverage designed to cover immediate medical expenses without determining legal liability, helping to prevent minor incidents from escalating into larger lawsuits. If a delivery person slips on a loose stair tread at your office and needs stitches, medical payments coverage could kick in quickly.

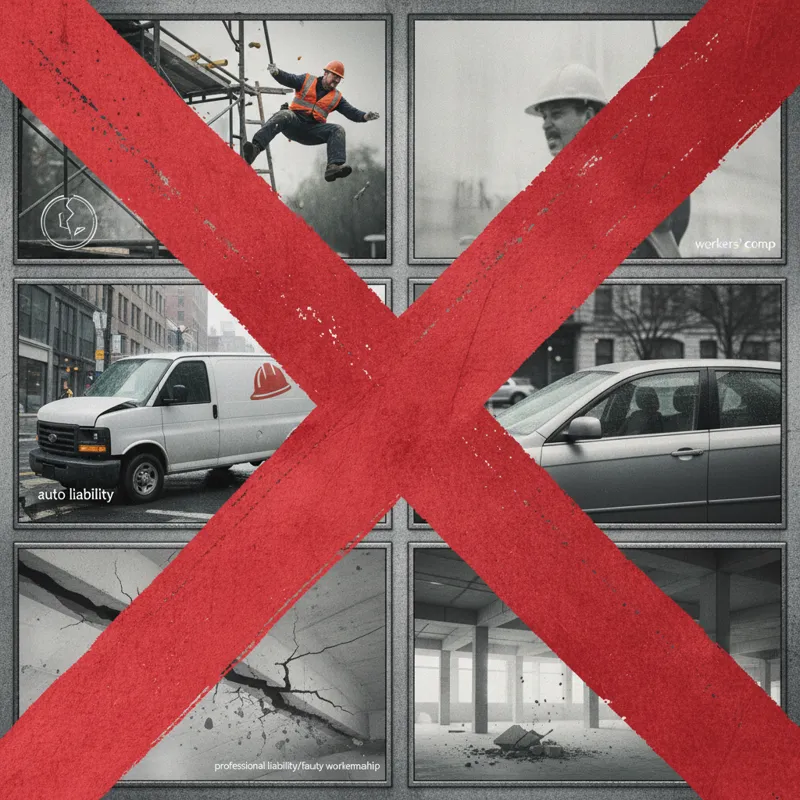

What General Liability Typically DOESN’T Cover

Just as important as knowing what your general liability insurance for contractors covers is understanding its limitations. This policy isn’t an all-encompassing shield for every possible business risk. Here are common exclusions:

- Employee Injuries (Workers’ Compensation): General liability doesn’t cover injuries to your own employees. For that, you need a separate policy: Workers’ Compensation insurance. Most states legally mandate this if you have employees.

- Professional Errors or Omissions (Professional Liability): If you provide advice, designs, or professional services (e.g., an architect or engineer acting as a contractor), and a client sues you for financial loss due to your faulty advice or error, general liability won’t cover it. That’s where Professional Liability (or Errors & Omissions) insurance comes in.

- Auto Accidents (Commercial Auto Insurance): Damage or injuries caused by your business vehicles are covered by Commercial Auto Insurance, not general liability. This includes company trucks, vans, and any vehicles used for business purposes.

- Faulty Workmanship: This is a big one. General liability policies typically exclude claims arising from faulty workmanship itself. If you build a leaky roof, the cost to repair or replace that roof isn’t covered. However, if that leaky roof causes water damage to the client’s expensive hardwood floors, the resulting property damage to the floors might be covered. It’s a nuanced distinction often misunderstood.

- Damage to Your Own Property: Your tools, equipment, and business premises aren’t covered by general liability. You’ll need a Commercial Property policy for these assets.

- Pollution Liability: Most standard general liability policies exclude claims related to pollution or environmental damage. If your work involves potential hazardous materials, you might need specialized environmental liability coverage.

- Contractual Liability: While complex, this generally refers to liability you assume under a contract that you wouldn’t otherwise have. Some contractual liability may be covered, but specific exclusions often apply.

Why Every Contractor Needs General Liability in 2026

In 2026, the reasons for securing adequate general liability coverage are more compelling than ever. It’s not just a “nice-to-have”; it’s fundamental for numerous practical and legal reasons:

- Legal Requirements: Many states and municipalities mandate that contractors carry general liability insurance to be licensed or even to pull permits. Operating without it could lead to fines, license suspension, or even being shut down. Staying compliant is non-negotiable.

- Client Demands: You’ll find that almost every reputable client, whether a homeowner, a business, or a general contractor, will require proof of your general liability insurance before you can even bid on a job, let alone start work. They need assurance that if something goes wrong, they won’t be left holding the bag.

- Financial Protection: Lawsuits are expensive. Even if a claim is frivolous, defending it can cost tens of thousands of dollars in legal fees. If you’re found liable, judgments can run into the hundreds of thousands or even millions. General liability insurance absorbs these costs, protecting your business assets from being wiped out.

- Peace of Mind: Knowing you’re covered allows you to focus on your craft. You can approach projects with confidence, knowing that unforeseen accidents won’t necessarily spell financial ruin. This peace of mind extends to your employees and partners as well.

- Reputation and Trust: Being properly insured signals professionalism and responsibility to clients, subcontractors, and partners. It builds trust, making you a more attractive and reliable business to work with.

Factors Influencing Your General Liability Insurance Premiums

The cost of a construction liability policy can vary significantly. Understanding what drives these premiums helps you manage costs and make informed decisions. When seeking contractor insurance quotes, expect insurers to consider these key factors:

- Type of Contracting Business: Roofing contractors or demolition specialists typically face higher premiums than, say, painters or landscapers, due to the higher inherent risks associated with their work. The more hazardous your trade, the higher the perceived risk for insurers.

- Location: Insurance rates can vary by state, county, and even city. Areas with higher populations, greater litigation rates, or specific environmental risks might see higher premiums.

- Claims History: A clean claims record will almost always result in lower premiums. Businesses with a history of frequent or costly claims will pay more, as they’re considered higher risk.

- Coverage Limits and Deductibles: Higher coverage limits (e.g., $2 million per occurrence instead of $1 million) will increase your premium. Conversely, choosing a higher deductible (the amount you pay out-of-pocket before insurance kicks in) can lower your premium, but you’ll bear more risk in the event of a claim.

- Number of Employees and Payroll: More employees generally mean more potential for incidents. Your total payroll is often a factor, as it’s an indicator of your business’s scale and activity.

- Subcontractor Exposure: If you frequently hire subcontractors, how you manage their insurance (e.g., requiring them to name you as an additional insured) can impact your rates. Insurers want to ensure that their liability isn’t absorbing risks that should be covered by others.

- Business Experience: Newer businesses might pay slightly higher rates initially until they establish a track record of safe operations and responsible management.

Determining the Right Coverage Limits and Deductibles

Choosing the correct coverage limits and deductibles for your general liability insurance for contractors isn’t a one-size-fits-all decision. It requires a thoughtful assessment of your specific business risks. Most standard policies offer limits like $1 million per occurrence and $2 million aggregate.

- Per Occurrence Limit: This is the maximum amount your policy will pay for any single incident or claim.

- Aggregate Limit: This is the total maximum amount your policy will pay out over the entire policy period (usually one year), regardless of how many claims occur.

Many contracts, particularly with commercial clients or general contractors, will explicitly require these minimums. However, depending on the scale of your projects and the potential for severe damage or injury, you might consider higher limits. For instance, a contractor working on multi-million dollar commercial projects may feel more comfortable with $2M/$4M limits, or even an umbrella policy to provide additional layers of protection. When considering deductibles, weigh the premium savings against your ability to pay out-of-pocket if a claim arises. A higher deductible means lower premiums, but you must be prepared to cover that initial expense. For a small business contractor, balancing these factors is crucial for both financial stability and adequate risk transfer.

The Importance of “Additional Insured” Endorsements

In the world of contracting, you’ll frequently encounter requests from clients, general contractors, or property owners to be named as an “Additional Insured” on your policy. This is a critical component of many construction contracts and a point of much discussion. An Additional Insured endorsement essentially extends some of your general liability coverage to another party. This means that if a claim arises from your operations and that third party (e.g., the property owner) is sued, your policy would respond to defend and indemnify them, often before their own insurance kicks in. This protects them from liability stemming from your work. It’s vital to understand the language used in these endorsements. Some might offer broad coverage, while others are very specific. You’ll often see requests for “primary and non-contributory” language, meaning your policy must pay first, and the additional insured’s policy won’t have to contribute unless your limits are exhausted. Failing to provide the correct endorsement can lead to contract breaches, delays, or even loss of a job. Always review these requests carefully with your insurance broker.

What Most Contractors Get Wrong About General Liability

After years in the industry, I’ve observed several common misunderstandings among contractors regarding their general liability insurance. These misconceptions can leave businesses dangerously exposed:

1. “I’m a small business, so I don’t need much coverage.”

Size doesn’t negate risk. A small, independent electrician can still cause a fire that destroys a client’s home, leading to a multi-million dollar claim. The potential for catastrophic loss exists regardless of your business’s scale. Adequate coverage isn’t about your size; it’s about your exposure.

2. “General liability covers everything that goes wrong on a job.”

As discussed, general liability has specific boundaries. It doesn’t cover employee injuries, professional errors, vehicle accidents, or damage to your own equipment. Relying solely on general liability leaves significant gaps in your protection. A comprehensive insurance program for contractors involves multiple policies.

3. “My faulty work will be covered if it causes damage.”

This is perhaps the most significant point of confusion. If your faulty workmanship itself needs to be fixed, general liability won’t pay for it. For example, if you install faulty plumbing, the cost to rip out and replace that plumbing is generally excluded. However, if that faulty plumbing then leaks and destroys the ceiling and furniture below, the consequential damage to the ceiling and furniture might be covered. The distinction is subtle but critical, and often the subject of intense legal debate.

4. “My subcontractor’s insurance protects me completely.”

While requiring your subcontractors to carry their own insurance and name you as an additional insured is a smart practice, it’s not a foolproof solution. If their limits are insufficient, or if their policy has exclusions that apply to the incident, you could still be on the hook. Your own general liability policy remains your primary defense for claims arising from your overall project management or direct actions.

5. “I just need the cheapest policy to get a contract.”

Focusing solely on price without understanding the coverage limits, exclusions, and endorsements can be a costly mistake. An underinsured policy might meet a contract’s basic requirement but leave you vulnerable to substantial out-of-pocket expenses when a large claim hits. Investing in proper coverage is investing in your business’s future. Just as some might research the 10 best sous vide cookers of 2026 for culinary perfection or delve into 10 proven best hair thickening products for personal care, understanding the specifics of your insurance is about careful selection, not just the lowest price.

How to Get the Best General Liability Insurance Quotes

Securing the right general liability insurance for contractors involves more than just picking the first quote you receive. Here’s a practical approach to finding the best coverage for your needs in 2026:

1. Prepare Your Business Information: Have details ready, including your business type, services offered, number of employees, annual revenue projections, past claims history, and desired coverage limits. The more accurate and detailed your information, the more precise your quotes will be.

2. Work with an Independent Insurance Agent: Unlike captive agents who work for a single insurance company, independent agents work with multiple carriers. This allows them to shop around on your behalf, comparing policies and prices from various providers to find the best fit for your specific contracting business. They can also offer invaluable advice on coverage nuances.

3. Compare Multiple Quotes: Don’t settle for just one quote. Obtain at least three to five quotes from different reputable insurers. When comparing, look beyond just the premium. Examine the coverage limits, deductibles, endorsements, and any exclusions. A slightly higher premium might come with significantly better protection.

4. Understand Your Policy: Before signing, thoroughly read and understand your policy documents. Ask your agent to clarify any terms, conditions, or exclusions you don’t fully grasp. Knowing what you’re covered for (and what you’re not) is crucial. Just as understanding the 7 proven benefits of Orange Pekoe tea enhances your appreciation of its qualities, a deep dive into your insurance policy ensures you leverage its full potential.

5. Review Annually: Your business evolves, and so should your insurance. Review your policy at least once a year, or whenever you take on new types of projects, hire more staff, or expand into new territories. Ensure your coverage remains adequate for your current risk profile.

Navigating Compliance: Legal and Client-Specific Requirements

For contractors, compliance isn’t a suggestion; it’s a mandate that impacts everything from project acquisition to legal standing. Your general liability insurance plays a central role here.

State and Local Licensing

Across the United States, state and local licensing boards often require proof of adequate general liability insurance to issue or renew a contractor’s license. These requirements vary significantly by jurisdiction and by the type of contracting work performed. It’s your responsibility to know the specific minimums for every area you operate in.

Client Contract Stipulations

Almost every professional contract you sign, particularly with larger clients, will detail specific insurance requirements. This includes minimum general liability limits, the need for additional insured endorsements, and sometimes even specific policy forms. Failing to meet these contractual obligations can lead to your bid being rejected, your contract being terminated, or even potential legal action if an incident occurs and your coverage is found lacking.

Bonding Requirements (Distinction)

While often discussed alongside insurance, it’s important to differentiate general liability from contractor bonds (like bid bonds, performance bonds, or payment bonds). Bonds essentially guarantee that you will fulfill your contractual obligations. They are not insurance in the traditional sense, as they don’t primarily protect you, but rather the client if you fail to perform. However, having robust general liability is often a prerequisite for obtaining certain types of bonds.

Always keep up-to-date Certificates of Insurance (COIs) on hand. These documents provide proof of your coverage to clients, general contractors, and regulatory bodies. Many clients will require these as a standard part of their vendor onboarding process.

FAQs about General Liability Insurance for Contractors

Here are answers to some of the most common questions contractors have about general liability insurance:

How much does general liability insurance for contractors typically cost?

The cost varies widely based on factors like your trade, location, claims history, and coverage limits. For a small, low-risk contractor, premiums might start from $400-$800 per year. Higher-risk trades or larger companies can pay several thousand dollars annually. Getting contractor insurance quotes tailored to your business is the best way to determine your specific cost.

Is general liability insurance mandatory for all contractors?

It depends on your state and municipality, and the type of work you do. Many jurisdictions legally require it for licensing and permitting. Even where not legally mandated, virtually all reputable clients will require it as a contractual condition. So, while not universally a legal mandate, it’s a practical and professional necessity for almost all contractors.

What’s the difference between general liability and professional liability insurance for contractors?

General liability covers claims of bodily injury and property damage resulting from your operations. Professional liability (or Errors & Omissions) covers claims of financial loss due to your professional mistakes, negligence, or bad advice. For example, a builder’s general liability covers if a ladder falls and injures a client; their professional liability would cover if a design flaw in their blueprint leads to a structural problem costing the client money.

Does general liability cover my tools and equipment?

No, general liability insurance does not cover your tools, equipment, or other business property. You’ll need a separate Commercial Property insurance policy, often included in a Business Owner’s Policy (BOP), or an Inland Marine policy for tools and equipment that are frequently moved between job sites.

Can I get general liability insurance if I’m a new contractor?

Yes, absolutely. New contractors can and should get general liability insurance from day one. In fact, many clients won’t even consider hiring a new business without proof of adequate coverage. Insurers are accustomed to underwriting policies for startups, though rates might be slightly higher initially until you establish a claims history.

How quickly can I get a certificate of insurance (COI)?

Once your policy is active, your insurance agent can typically issue a Certificate of Insurance (COI) very quickly, often within minutes or a few hours, especially if it’s a standard request. For more complex endorsements, it might take a day or two. Always communicate your needs clearly to your agent.

As a contractor, your business is built on trust, skill, and reliability. Protecting that business with the right General Liability Insurance for Contractors is not merely a formality; it’s a strategic decision that safeguards your financial future and enhances your professional standing. In 2026, with increasing complexities in regulations and client expectations, having robust general liability coverage is more critical than ever. Don’t leave your business exposed to unnecessary risks. Take the proactive step to review your current coverage or get competitive quotes today.

General Information & Professional Disclaimer

Disclaimer

The information provided by bangladeshcountry.com (“we,” “us,” or “our”) on our website is for general informational purposes only. All information on the Site is provided in good faith; however, we make no representation or warranty of any kind, express or implied, regarding the accuracy, adequacy, validity, reliability, availability, or completeness of any information on the Site.

Not Professional Advice The Site cannot and does not contain financial, insurance, legal, medical or professional career advice. The insurance related information is provided for general informational purposes only and is not a substitute for professional advice.

We are not certified financial advisors, insurance agents, or legal professionals. Accordingly, before taking any actions based on such information, we strictly encourage you to consult with the appropriate professionals or certified authorities. We do not provide any kind of professional or financial advice.

THE USE OR RELIANCE OF ANY INFORMATION CONTAINED ON THIS SITE IS SOLELY AT YOUR OWN RISK. We shall not have any liability to you for any loss or damage of any kind incurred as a result of the use of the site or reliance on any information provided on the site.